If you’re SaaS, tech, or growth company, you can access debt funding through different kinds of funding instruments and debt providers. Leading examples include re:cap, Gilion, Tapline, and Riverside. They offer debt funding for such businesses, matching various use cases, growth stages, and requirements.

When a SaaS or tech founder walks into a traditional bank, they often leave empty-handed. Not for lack of financial discipline, but because banks expect tangible collateral (think: machinery, property, inventory).

What they find instead is a codebase and a subscription model with steady revenue, but few physical assets to take in default.

Why startups turn to debt lenders

This mismatch leaves a capital vacuum. Recurring revenues suggest dependable cash flow. Yet lenders trained in industrial-era economics remain reluctant to extend credit to software-heavy companies.

However, timing and preparation open doors even for SaaS and tech companies. As Rob Morelli of Overlap Holdings recently wrote:

“The less you need [debt], the easier it is to get...Lenders are most eager to work with companies that are growing and have plenty of runway.”

Apply for debt when you don’t need it

In other words: apply for debt when you’re strong and don’t wait until you're desperate. Have clean financials, a clear repayment plan, forecasts grounded in realistic assumptions, and know your numbers by heart.

Don’t pitch like you’re selling the next unicorn. Pitch like you’re a reliable borrower and are able to pay back debt and interest.

Fortunately, a new class of debt providers has emerged. They analyze your company based on metrics essential for SaaS and tech businesses (MRR, churn, runway, recurring revenue) rather than square footage or production output. They offer non‑dilutive capital: revenue‑based financing, venture debt, or revolving credit lines tailored for the digital age.

In this article we explore different debt funding providers for SaaS, growth and tech companies. All of them understand how these businesses operate and offer capital solutions without asking for shares or asset-heavy collateral.

Secure debt funding designed for SaaS and tech companies

Find out if your company is ready for debt financing in 60 seconds

Check fundability nowOverview: Debt lenders for startups

- re:cap

- Gilion

- Riverside

- Tapline

- BackRock Venture & Growth Lending (formerly Kreos Capital)

- Columbia Lake Partner

- Atempo

What is debt funding for startups?

Debt can help companies grow without giving up more equity. For founders, this means they keep more control and avoid dilution at early stages. Non-dilutive capital is often cheaper than equity in the long run (think: implicit and explicit cost of capital).

A lot of tech and SaaS businesses have recurring revenue and predictable cash flows. This makes them better suited for debt funding. They are more likely to repay it over the long-term due to a stable customer base and long-lasting contracts.

How to qualify for debt funding as a startup

Not every SaaS and tech company will qualify for debt funding. Lenders and alternative finance providers look for predictable, stable cash flows that signal you can repay the capital plus interest.

In short, qualifying for debt funding means showing that your SaaS business is stable, predictable, and ready to scale, without putting your runway or repayment ability at risk.

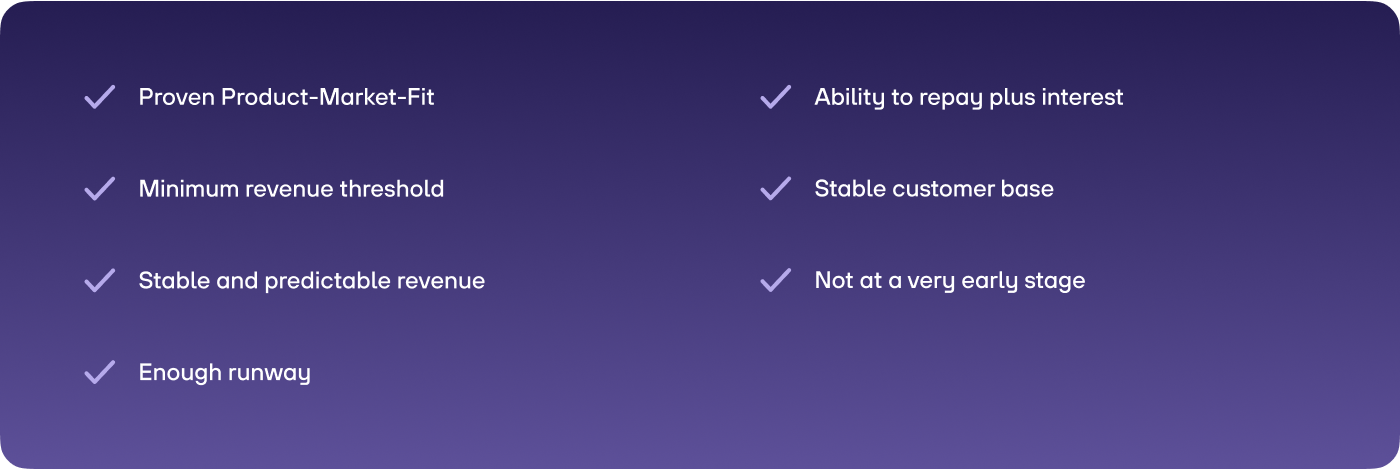

Here’s what you typically need to show:

1. Proven Product-Market Fit

You should have already found product-market fit (PMF). If you’re still pivoting your core offering or business model, lenders will see you as too high risk. Debt providers prefer companies that are scaling an established product, not experimenting with unproven ideas.

2. Minimum revenue threshold

Most debt funding providers want to see at least €250k-€500k in annual recurring revenue (ARR). Some venture debt lenders may require €1M+ ARR, depending on ticket size. This shows you have real traction and a revenue engine that works.

3. Stable and predictable revenue

Your revenue streams should be recurring and predictable. A steady customer base with low churn and multi-month or annual contracts is ideal. One-off sales or unpredictable spikes make it harder to model repayments.

4. Enough runway

Debt funding works best when you’re not desperate. You should have enough cash runway already, at least 6-12 months, to avoid over-leveraging. Lenders want to see that you won’t instantly burn through the funds.

5. Ability to repay plus interest

Unlike equity, debt must be paid back. Providers will analyze your gross margins, burn rate, and growth plans to check whether you can comfortably make repayments plus any interest or fees without harming day-to-day operations.

6. Stable customer base

A healthy, diversified customer base reduces risk. If your revenue depends heavily on one or two large clients, it’s a red flag. Lenders prefer companies with many customers paying reliably.

7. Not at a very early stage

Debt funding isn’t usually an option for pre-revenue or pre-seed startups. Most lenders want to see that you’ve moved beyond MVP stage and are generating consistent monthly revenue with some growth momentum.

Debt funding use cases for startups

Grow into profitability

Startups often use debt to grow into profitability. Many startups underestimate how much time it takes to reach profitability. Monthly costs run ahead of revenue, and growth demands upfront spend. Debt funding can be used as bridge financing, so teams do not have to raise new equity too early or at weak valuations.

Postpone equity fundraising

Some companies use debt to postpone their next equity round. With enough runway, they can show stronger numbers and better KPIs. This often means they raise at higher valuations and give up less ownership.

Cover large one-time expenses

Debt can also help finance large one-time investments. For example, a company might use debt to fund an acquisition that adds new revenue streams. Other teams use it as growth capital to launch major marketing campaigns or expand into new markets. Instead of taking a large equity round for every new growth push, they spread out costs over time and match repayments to incoming cash.

Working capital

Debt can be a smart way to smooth out the day-to-day ups and downs of running a SaaS or tech business. Even with recurring revenue, unexpected delays in customer payments, seasonality, or upfront costs for onboarding new clients can create short-term cash gaps.

A revolving credit line or short-term loan gives you the flexibility to cover your day-to-day without draining reserves. Used well, working capital financing keeps your operations running smoothly and your team focused on growth.

Growth financing

Many SaaS and tech companies use debt strategically to accelerate growth that would otherwise take too long to fund through operating cash flow alone. This could mean scaling your sales team faster, investing in product development, or expanding into new markets.

Because these investments often pay off over time, growth financing lets you match the upfront spend with the extra revenue it generates. The result: you reach key milestones sooner, hit better metrics for your next funding round, and strengthen your market position.

Used well, debt is a tool to gain time, stay in control, and keep the cap table lean. The key is to take on debt when the business is strong enough to pay it back comfortably.

What kind of different instruments are at your disposal?

Which debt funding instruments are relevant for startups?

The most common debt instruments for SaaS and tech companies are revenue-based financing, venture debt, and flexible credit lines. All of them are provided by specialized financial institutions (e.g. Fintech or Funds).

Revenue-based financing ties repayments to a percentage of monthly revenue. Venture debt is often structured like a term loan and works well alongside venture capital. Credit lines can be revolving or flexible, giving founders cash when needed without upfront lump sums.

Let’s take a closer look at these debt funding instruments.

1. Revenue-based financing (RBF)

What it is

Revenue-based financing ties repayments directly to your company’s monthly revenue. You get an upfront cash advance, and repay it as a fixed percentage of your future monthly income until the total agreed amount is repaid, plus a flat fee or factor rate.

According to various studies, the global RBF market reached a total volume of $5.78B in 2024. It's projected to reach more than $40B by 2028.

How it works

Repayments rise and fall with your revenue. If sales drop, payments shrink. If sales increase, you repay faster. No fixed interest, no fixed term.

Benefits

- No equity dilution

- Payments flex with your cash flow

- Often faster to arrange than a bank loan

- No hard collateral required

Cons

- Total cost can be higher than a standard term loan if your revenue spikes

- Some providers cap advance rates at around 30-50% of ARR

- Not ideal for companies with volatile or seasonal revenue swings that dip too deep

2. Venture debt

What it is

Venture debt is a term loan designed to complement venture capital. It’s typically available to companies that have already raised VC equity. The debt comes with a fixed interest rate and a defined repayment schedule, usually 12-36 months.

According to the Global Venture Debt Report 2025, venture debt is gaining more traction among founders. The deal volume has grown around 14% CAGR from 2018 to 2024. In 2024 venture debt deals with a volume of $83.4B were closed.

How it works

Lenders look at your VC backing and growth trajectory rather than physical collateral. Some loans include warrants that give the lender the right to buy equity at a later stage.

Benefits

- Extends runway between equity rounds

- Cheaper than raising the same amount in new equity

- Helps improve cash buffer without immediate dilution

Cons

- Often includes covenants on revenue, profitability, or cash balance

- May require small equity warrants, adding mild dilution

- Failure to meet covenants can trigger early repayment

3. Term loan

What it is

A traditional term loan is a lump sum borrowed upfront with a fixed interest rate, repaid in equal installments over a set period.

How it works

Repayment is fixed, so you know your cash outflow in advance. Unlike RBF, payments do not flex with revenue. Some term loans for SaaS come with flexible terms if the company is well-established.

Benefits

- Predictable cost and timeline

- Can be cheaper than RBF for stable, mature companies

- Often lower total cost than venture debt if no warrants

Cons

- Payments stay the same even if your revenue dips

- May require personal guarantees or security

- Very hard to negotiate for early-stage, asset-light startups

- Most traditional banks can’t underwrite or assess early-stage tech or SaaS businesses

4. Revolving credit line

What it is

A revolving credit facility works like an overdraft or a company credit card. The lender sets a credit limit. You draw funds when needed and repay them flexibly. You only pay interest on what you use.

How it works

Draw and repay as needed, reuse as many times as you want within the term. Often used for short-term working capital or to cover lumpy expenses.

Benefits

- Maximum flexibility

- Only pay for what you use

- Good for smoothing seasonal or cyclical revenue

Cons

- May come with commitment fees even if unused

- Interest rates can be higher than term loans for the same amount

- Not suited for large one-time growth investments

5. Flexible credit line

What it is

Similar to a revolving credit line but designed specifically for SaaS. Providers assess your ARR and set a limit you can draw from. Some fintech lenders in Europe offer these as an always-on facility to help manage cash gaps.

How it works

Draw funds as needed. Repay and re-borrow as your needs change. Often integrated with revenue metrics so limits adjust automatically.

Benefits

- Combines predictability with flexibility

- Tied to real-time performance

- Works well for covering unexpected expenses or short-term scaling

Cons

- Lower limits than lump-sum venture debt

- Interest costs can add up if overused

- Requires strong revenue reporting and forecasting

10 questions a startup must ask its lender

These questions cut to the heart of what makes one offer better than another. They expose: actual cost vs. headline rate, flexibility in tricky months, strings attached via covenants or warrants, administrative effort, and commitment of the debt funding provider.

1. What is the full cost of capital?

Ask for all-in figures: interest rates, one-off fees, other fees, repayment caps, warrants. Drill into APR or factor rate to compare evenly.

2. What advance rate or credit limit will you provide?

Find out how much of your ARR or MRR you can draw. For example, RBF providers often limit this to 30-50% of ARR.

3. How flexible are repayments?

Will repayments adjust monthly with revenue? Can you skip or reduce payments during slow months? Are there grace periods? Essential for managing seasonal or volatile cash flow.

4. What covenants, triggers, or default conditions apply?

Identify minimum MRR, cash balance, growth milestones that you must maintain, and what happens if you fail .

5. Is there an equity kicker like warrants?

Venture debt often includes warrants (~5-20%). Ask how they work, vest, and convert and whether full repayment avoids warrants

6. What is the term length and repayment schedule?

Clarify interest-only periods, amortization, balloon payments, or revolver expiry. Funds drawn too early can harm the runway if repayments start later.

7. Can I prepay or refinance early?

Ask if early repayment is allowed and if any penalties or fees apply; also whether you can top up your facility later.

8. How long will funding take?

Understand the timeline:

- Initial talk

- Term sheet

- Underwriting

- Funding

Ask specifically about each stage’s typical duration. If you want to know how long it takes with re:cap, here’s a detailed funding process with the single steps.

9. What reporting or board rights will I need to comply with?

Check administrative burden: regular financial reporting, board meetings, and any requirement for board seats.

10. What is your track record with companies and handling downturns?

Ask for references, especially companies that hit slower growth, and understand how lenders have responded in hard times.

Summary: Debt lenders for startups

Debt funding has matured into a serious growth lever for SaaS, tech, and digital-first businesses.

Founders don’t have to rely solely on equity and dilution. They can combine revenue-based financing, venture debt, or flexible credit lines to extend runway and strengthen negotiating positions.

But the same rule holds true everywhere: use debt to build momentum, not to plug holes in a sinking ship.

The best time to secure debt is when you have stable revenues, a clear plan, and enough cash runway to repay it comfortably. That’s when lenders trust you and when debt works for you, not against you.

As more specialized providers like re:cap, Gilion, Riverside, and Tapline enter the market, founders finally have access to lenders who understand recurring revenue, customer retention, and subscription economics.

That’s why it’s important to compare the different offers available.

If you do your homework, keep your metrics in shape, and ask the right questions, debt can be a powerful, non-dilutive tool to reach the next stage on your terms.

Q&A: Debt lenders for startups

What is debt funding for SaaS or tech companies?

Debt funding means a SaaS or tech company borrows money from a lender, like a bank, venture debt fund, or revenue-based financing provider, and repays it over time with interest, without giving up equity.

How does revenue-based financing work for SaaS and tech companies?

With revenue-based financing (RBF), a SaaS or tech company gets upfront capital in exchange for a fixed percentage of future monthly revenues until a repayment cap is met. It’s popular for recurring-revenue models.

Who provides venture debt for SaaS or tech businesses?

Global examples include Silicon Valley Bank, TriplePoint Capital, Claret Capital, and many regional venture debt funds. Fintechs like re:cap, Gilion, or Tapline offer flexible credit lines or other debt funding models.

What are typical requirements to get debt funding as a SaaS or tech company?

Most lenders look for steady recurring revenue (ARR), low churn, positive unit economics, and predictable cash flow. Venture debt often requires recent VC funding.

What’s the difference between debt and equity funding for SaaS and tech?

Debt funding means repaying a loan plus interest, with no ownership dilution. Equity funding means raising capital by selling shares, which reduces your ownership stake but doesn’t need repayment.

Can early-stage SaaS and tech startups get debt funding?

It’s possible, but options are limited. Most providers prefer a proven revenue track record, stable customer base, and PMF. A typical minimum is around €500k-€1M in ARR.

Why do SaaS and tech companies use debt funding?

Debt funding can help extend runway, invest in growth, or smooth cash flow without diluting ownership. It’s often used to bridge the gap between equity rounds or to finance predictable growth.

How do I choose the right debt funding option for my business?

Compare different providers on factors like ticket size, repayment structure, interest or fees, required covenants, eligibility criteria, and how well they understand subscription revenue models.

Where can I find a list of debt funding providers relevant for SaaS and tech companies?

Check online funding marketplaces, industry reports, or guides like this one. Many specialized fintech lenders and venture debt funds publish their terms and requirements transparently.

Secure debt funding designed for SaaS and tech companies

Find out if your company is ready for debt financing in 60 seconds

Check fundability now