What is a business loan? (and how it fuels growth)

In business, access to capital often makes the difference between scaling up and falling behind.

Whether you’re a startup looking for funding or an established company planning an expansion, a business loan is one of the most common and flexible funding tools available.

But not all business loans are created equal, and understanding how they work is key to choosing the right one.

In this guide, we break down what a business loan is, how it works, and when it makes sense to use one.

Business loan: definition

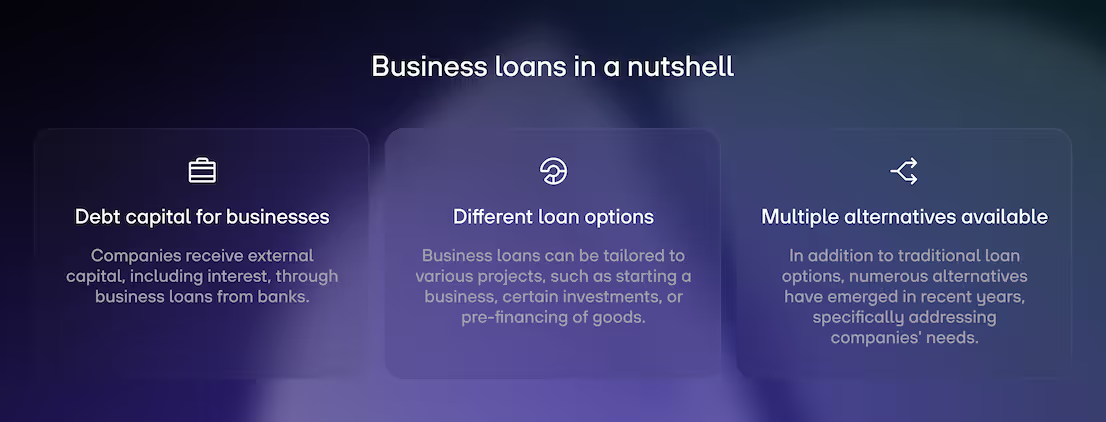

A business loan is a lump sum of money that a company borrows from a financial institution (typically a bank, credit union, or lender) with the agreement to repay it over time, with interest.

Business loans are used to cover a wide range of needs, from day-to-day operations to major investments in growth.

Business loans can be categorized by

Business loans represent the most widely used form of external capital acquisition. In 2022, banks granted €1.8 trillion in loans to companies and self-employed individuals in Germany. The majority of these are small business loans.

What can a business loan be used for?

Business loans are flexible and can serve many financial goals:

- Working capital: smooth out cash flow during slow periods

- Hiring or payroll: fund new roles or seasonal staff

- Expansion: open new locations or enter new markets

- Equipment & inventory: upgrade machinery or restock ahead of demand

- Bridge financing: cover short-term gaps before incoming revenue or equity rounds

The right business loan allows you to invest in your company’s future without giving up equity or diluting ownership.

Why choose a business loan?

Business loans offer several strategic advantages over other financing options:

The terms you receive often depend on your relationship with the lender, financial track record, and collateral (if applicable). Strong financials = lower interest rates and better flexibility.

Secure your next funding – without giving up equity

Get up to €5M in non-dilutive funding with re:cap. Calculate your funding terms and see how much growth capital you could get.

Calculate funding termsWhat are key components of a business loan?

A business loan is an agreement between a company and a bank. The key components may vary depending on the lender and the type of loan. Here are some commonalities:

Core elements of a business loan

Always review the loan agreement thoroughly. Watch out for fees, penalties, and early repayment terms.

How to apply for a business loan (step-by-step)

Securing a business loan is more than filling out a form. It’s a strategic process that starts with preparation and ends with a signed contract.

Here's how the application process works

- Preparation: before applying for a loan, businesses should prepare a detailed business plan, financial statements, and cash flow projections.

- Choosing the right Loan: companies must assess their financing needs and select the appropriate type of loan. Factors to consider include the loan amount, repayment terms, interest rates, and collateral requirements.

- Finding a lender: businesses can approach traditional banks, credit unions, online lenders, or alternative financing institutions.

- Application submission: the application process involves submitting the necessary documentation, such as financial statements, tax returns, business licenses, and personal identification. Then, lenders conduct a credit analysis.

- Approval and disbursement: once approved, the lender will issue a loan agreement detailing the terms and conditions. Upon signing, the loan amount is disbursed, and the business can begin using the funds.

.avif)

What are different types of a business loan?

Various types of loans fall under the category of business loans. Usually, banks offer business loans. However, there are other institutions providing debt financing for companies.

Term loan

These are traditional loans where a business borrows a lump sum and repays it over a set period with interest. They can be short-term (less than a year), medium-term (1-5 years), or long-term (over 5 years). Term loans are commonly used for major capital expenditures, expansion, or large projects.

Lines of credit

A line of credit provides businesses with flexible access to funds up to a certain limit. Interest is only paid on the amount borrowed. This type of loan is ideal for managing cash flow and covering short-term operational needs.

Loan for starting a business

A startup can access a wide range of financing instruments, both debt or equity. Besides venture capital, bootstrapping, or angel investors, they can get specific startup loans from traditional banks.

Such a loan is suitable for:

- Startups with a classic business model that banks can reflect and understand with their risk model.

- Startups with an innovative business model that already generates revenue and is preferably profitable.

- Startups that can take debt and repay it, including interest and installment payments.

- Startups that don’t want to dilute their shares and stay independent.

A loan for starting a business provides planning security for young companies. They know exactly which capital costs occur and when.

However, access to credit is difficult for many startups, especially those in the tech and SaaS industries. They can hardly offer any collateral, such as real estate or machinery. They also have a business model outside the scope of a bank's risk analysis.

Investment loan

Companies can use an investment loan to finance long-term growth measures or projects. Usually, this includes traditional tangible assets such as production facilities, infrastructure projects, machinery, or real estate.

In contrast to an overdraft facility (working capital), which primarily covers ongoing costs, the credit line of an investment loan is intended to advance a company over the long term. Therefore, the duration is up to ten years in some cases.

Investment loans are tied to a specific purpose. A clear definition of the intended use enables a bank to better assess its risk.

Earmarked lending does not only include infrastructure projects for manufacturing companies, though. It also covers project financing for service providers such as agencies, consultancies, or other professional services. They use loans, for example, to finance large individual expenses (hardware or events).

Here's an example of Dutch company Stories, who has used the credit line from re:cap to refinance it's operational expenses for further growth.

Bank guarantee

A bank guarantee is not a traditional business loan where a company receives debt from a financial institute. The bank guarantees a company to a third party and receives a commission. Interest or repayment installments are not included.

Suppliers and service providers, for example, often ask for a bank guarantee before they provide their services. It secures their risk in the event payment defaults. The bank guarantees that the company is financially able to meet the claim.

Goods financing

With goods financing, a company receives a loan to purchase goods or raw materials, which are resold at a profit. This type of business loan is also known as goods pre-financing or purchase financing.

Goods financing is particularly relevant for companies active in retail or e-commerce and regularly require large quantities of goods to run their business.

Commodity financing instruments include:

- Letter of Credit, which is issued by a bank and guarantees payment to the seller once certain conditions are met.

- Documentary Collection: This is a payment arrangement where the buyer's bank processes the payment once the required trade documents are presented.

- Supplier credit: suppliers grant buyers a temporary loan to pay for goods.

Goods financing is an important instrument for bridging financial bottlenecks in terms of liquidity. This is especially true when companies need to purchase large quantities of goods, but payment is only made after a certain period.

Overdraft facility

The overdraft facility is also known as a working capital or operating loan.

It provides companies with short-term liquidity to finance ongoing expenses. This type of business loan enables companies to react to fluctuations in their capital requirements and to bridge short-term financial bottlenecks.

The most important aspects of an overdraft facility are

- Flexibility in obtaining liquidity: an overdraft facility is a flexible form of financing that allows companies to withdraw money from their bank account up to a pre-agreed maximum amount.

- Short-term financing: Overdraft facilities are designed for short terms, often for one year or less.

- Risk management: Companies should practice effective risk management to prevent short-term debts from turning into long-term financial burdens.

Alternatives to a traditional business loan

Traditional bank loans may not be ideal for all companies. Some startups, especially in the tech and SaaS sectors, face challenges with traditional business loans from banks.

Such alternative instruments include:

- Factoring

- Leasing

- Convertible loans

- Venture debt

- Alternative debt funding

- Revenue-based financing

- Recurring revenue financing

These alternatives, often offered by fintechs, online lenders, or funds, allow companies to diversify their capital structure beyond traditional routes.

They leverage automation and risk assessment based on real-time financial data and specific SaaS- and Tech-KPIs, providing more accurate capital solutions with flexible terms.

The advantages of alternative financing:

- Companies have more freedom as the capital is not tied to a specific purpose.

- Companies gain a high degree of flexibility as there are no rigid repayment models, and debt can be taken more easily.

- Companies have access to real-time data on their financial performance. This allows them to react to problems at an early stage.

What are benefits of a business loan?

What are risks of a business loan?

Final takeaway: business loans

A business loan is one of the most widely used and flexible tools for funding operations, growth, or investments. It offers structure, predictability, and ownership retention but comes with responsibilities.

The key is fit:

- Right loan type

- Right lender

- Right timing

- Clear understanding of your repayment ability

With smart planning and strong financials, a business loan can help your company scale sustainably.

Summary: business loan

- A business loan gives companies access to capital for growth, working capital, or strategic investment.

- Common types include term loans, credit lines, investment loans, and overdrafts.

- Modern alternatives (like RBF or venture debt) offer flexibility for startups and SaaS companies.

- Benefits: capital access, control retention, and tax advantages.

- Risks: repayment pressure, debt burden, and cash flow constraints.

- Smart financing starts with clear goals, the right funding structure, and lender fit.

Secure your next funding – without giving up equity

Get up to €5M in non-dilutive funding with re:cap. Calculate your funding terms and see how much growth capital you could get.

Calculate funding terms