What is Factoring? (The Strategic Tool for Cash Flow and Working Capital Optimization)

For businesses reliant on invoicing, the gap between delivering a service or product and receiving payment (often 30, 60, or even 90 days) creates a perpetual cash flow problem. This lag locks up essential capital, hindering growth.

Factoring (also known as Accounts Receivable Financing) is a powerful financial solution where a business sells its outstanding invoices (receivables) to a third party (the Factor) at a discount in exchange for immediate cash.

It is no longer a last resort; factoring has become an established, non-dilutive, and highly scalable Working Capital Management (WCM) instrument used across manufacturing, logistics, staffing, and technology sectors.

In this comprehensive guide, you’ll learn:

- The Mechanics of Factoring: How the process works and its core financial components (Advance Rate, Discount Fee).

- The Strategic Types: When to use Recourse vs. Non-Recourse factoring.

- Factoring’s Role in WCM: How it directly impacts the Cash Conversion Cycle (CCC).

- Cost Analysis and Risk Mitigation: Calculating the true cost of factoring.

- Industry Applications: Why factoring is crucial for high-growth, long-payment cycle businesses.

Factoring: Definition

Factoring is a type of short-term financing where a business sells its accounts receivable (e.g., unpaid invoices) to a third party, called a factor, at a discount. In return, the company gets immediate cash instead of waiting for customers to pay. It's an alternative way of funding a company.

Key benefits of factoring

- Immediate access to cash (usually within 24-48 hours)

- Improved working capital and liquidity

- No need to wait for long invoice payment terms

- Outsourced receivables management

Unlike debt collection agencies (which act after payment is overdue), factoring happens proactively, right after an invoice is issued.

This article will explore the concept of factoring in depth, discussing its mechanisms, benefits, risks, types, and applications in various business contexts.

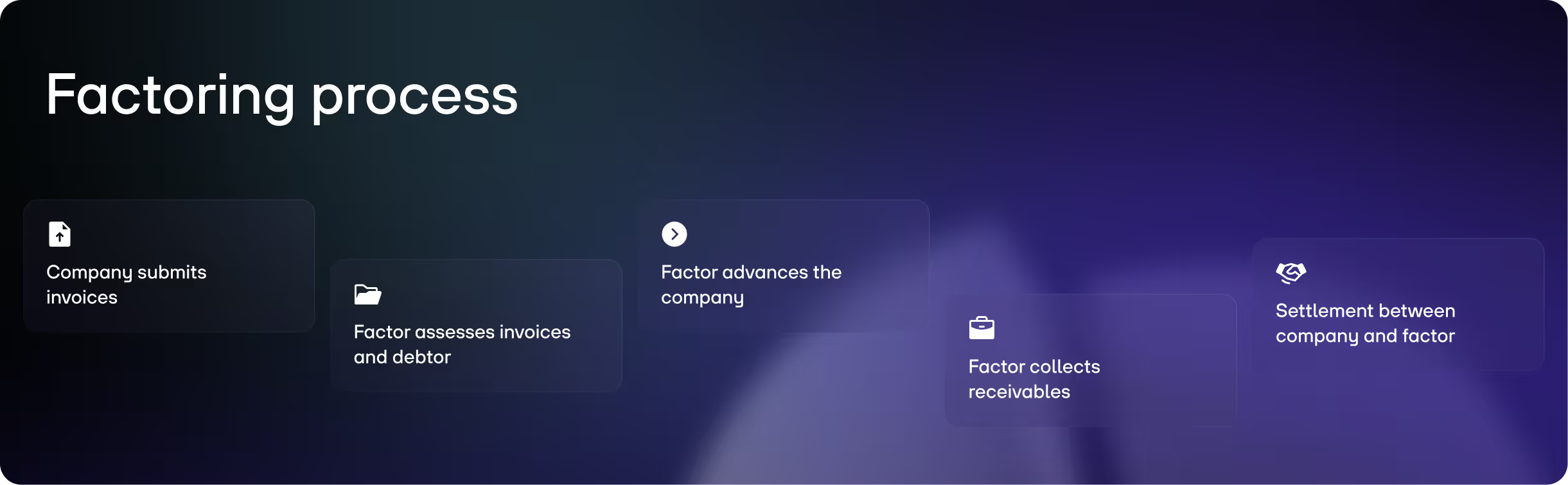

How does factoring work? (step-by-step)

Factoring involves three key parties:

- The company is seeking to convert its accounts receivable into cash.

- The factor acquires the outstanding receivables from the company and provides immediate capital.

- The customers of the company (debtor) who owe the company payments for outstanding invoices.

This is a typical factoring process – in simple terms

What does factoring cost?

Factoring fees are typically structured in two parts:

- Service fee: A percentage of the invoice amount (e.g. 1-3%), covering receivables management, credit checks, and risk protection

- Financing interest: Charged on the advance provided until the invoice is paid in full

What does this look like in a concrete example?

Factoring example calculation

Suppose a company has outstanding receivables totaling €500,000. In order to obtain liquid funds quickly, it assigns its receivables to a factor. The factor estimates the following costs:

As a result, €400,000 are directly available to the company. This advance payment is usually available within 24-48 hours. The company does not have to wait several weeks or months for it - and can deploy this money immediately.

Types of factoring

Factoring is highly flexible and can be tailored to a company's needs and goals. Several types of factoring are generally available:

Full Service Factoring / Recourse Factoring

All in one solution: With full service factoring, companies hand over all factoring processes to the factor.

They sell the receivable, outsource dunning and collection, and take out 100% protection against payment defaults (del credere clause).

This type of factoring is considered standard among factoring companies and financial service providers.

Companies not only receive liquidity, but also relieve their accounting system and protect themselves against payment difficulties or defaults. Full service factoring is also called recourse factoring.

Non-recourse Factoring

In non-recourse factoring, a factor performs the same services as in full service factoring – with one exception: the factor does not bear the default risk. This remains with the company.

This is particularly suitable for companies that have an established customer base and long-term relationships with their customers.

Usually, these companies are in a good position to assess the solvency of their customers.

Secure your next funding – without giving up equity

Get up to €5M in non-dilutive funding with re:cap. Calculate your funding terms and see how much growth capital you could get.

Calculate funding termsNotification Factoring

Open factoring is characterized by transparency - especially for the company's debtors. They are instructed to transfer the outstanding receivables to the factor rather than the company.

In the past, companies were still reluctant to use open factoring. This has now changed. Factoring has become established as an alternative financing model.

Non-notification Factoring

However, if companies have concerns about their customer relationships, they can also use silent or non-notification factoring.

In this case, the debtors are not informed that the company has assigned its receivables to a factor.

The invoice shows the "regular" company as the payment recipient. The "regular" company also receives the money but transfers it directly to the factoring company.

Due date Factoring

With due date factoring, the factoring company only takes over the receivables collection at the due date. The receivable is not pre-financed by the factor, which only assumes the risk of non-payment.

Section Factoring

A company wants to sell only a part of its outstanding receivables. Then selective factoring is the way to go (also cut-out factoring).

The company decides which invoices to refinance using factoring, for example, from a specific customer group (major customers with high outstanding amounts or a negative payment history).

In-house Factoring

In comparison to comprehensive full-service factoring, in-house factoring involves the company retaining control over receivables management, encompassing the dunning and collection processes.

In this scenario, the factor's role is primarily limited to financing the receivables and managing default protection.

Domestic Factoring

This type of factoring involves all parties (the business, the factor, and the customer) being located in the same country. Domestic factoring is simpler and involves fewer legal and regulatory complications compared to international factoring.

International Factoring

International factoring occurs when the business, factor, and customer are located in different countries.

This type of factoring helps businesses manage the complexities of cross-border transactions, such as foreign exchange risk and differing legal systems.

Benefits of factoring

Improved cash flow

Factoring provides businesses with immediate cash, improving liquidity and enabling them to meet short-term financial obligations, such as paying suppliers and employees. This is especially crucial for businesses with long payment terms or those experiencing rapid growth.

Invest in growth

Improved liquidity allows the company to invest in further growth.

Enhanced working capital management

Factoring helps businesses manage their working capital more effectively by converting accounts receivable into immediate cash. This can improve the company's overall financial health and facilitate investment in growth opportunities.

Reduction of Bad Debt Risk

Non-recourse factoring transfers the risk of bad debts to the factor, protecting the business from potential losses due to customer non-payment. This allows businesses to focus on their core operations without worrying about the creditworthiness of their customers.

Simple receivables management

Factors typically handle the collection of invoice payments, relieving businesses of the administrative burden and costs associated with managing accounts receivable. This can lead to more efficient and professional debt collection.

Fast and convenient

Factoring is usually faster and easier for a company than accessing a traditional financial instrument, such as a bank loan.

Flexibility and scalability

Factoring is a flexible financing option that grows with the business.

As sales and accounts receivable increase, the amount of financing available through factoring also increases. This makes it an ideal solution for companies experiencing seasonal fluctuations or rapid growth.

Risks of factoring

Cost

Factoring can be significantly more expensive than other financing methods because the factor charges a fee for its service.

The fees charged by factors, which can include advance fees, discount rates, and service fees, may add up and affect the overall profitability of the business.

Dependent on customer creditworthiness

The terms and availability of factoring depend heavily on the creditworthiness of the business's customers.

If customers have poor credit ratings or a history of late payments, the factor may offer less favorable terms or decline to provide financing altogether.

Potential impact on customer relationship

The involvement of a third party in the collections process may impact customer relationships, particularly if the factor employs aggressive collection tactics.

Businesses must choose factors that align with their customer service philosophy to mitigate this risk.

When is factoring the right financing instrument?

Factoring is a suitable financial solution for different businesses, including startups, small and medium-sized enterprises (SMEs), and freelancers.

It's particularly beneficial for businesses that have already delivered their services at the time of invoicing and face challenges such as:

- A significant volume of outstanding receivables and high inventory levels.

- Long payment terms that hinder cash flow.

- An ongoing need for liquidity to fuel further growth.

- High acquisition costs for materials and machinery.

Factoring has established itself as an alternative financial instrument for companies. In 2022, the revenue of the German factoring industry was around €373 billion – an increase of 137% compared to 2012.

According to the German Factoring Association, the market penetration of factoring in this country is around ten percent.

In a European comparison, however, penetration is low. For example, Belgium (18%), Spain (16%), Portugal (15.5%) or France (14%) have higher figures.

Applications of Factoring Across Diverse Industries

Factoring is not limited to financially distressed companies; it is a vital liquidity tool for industries facing specific structural cash flow challenges.

Factoring for financing a company

Non-bank financing methods have become increasingly crucial for companies. Factoring is such an alternative to traditional sources of financing – and has gained in importance in recent years.

Companies that rely exclusively on factoring have almost no outstanding receivables. In this way, they protect their liquidity and equity - which also makes it easier to obtain a bank loan again.

As a versatile financial instrument, factoring can seamlessly integrate into a company's accounts receivable management, offering various factoring models to choose from, each with different levels of service.

This adaptability makes it a valuable resource for businesses seeking financial flexibility and growth opportunities.

Applications of factoring in various industries

Manufacturing

Manufacturers often face long payment terms from retailers and distributors, creating cash flow challenges.

Factoring allows manufacturers to convert their accounts receivable into immediate cash, enabling them to purchase raw materials, pay wages, and invest in production capacity.

Transportation and logistics

The transportation and logistics industry frequently deals with delayed payments from clients.

Factoring provides companies with the necessary liquidity to cover fuel costs, maintenance, and payroll, ensuring smooth operations and growth.

Staffing agencies

Staffing agencies must pay their employees regularly, even if clients take longer to pay their invoices.

Factoring helps staffing agencies bridge the gap between paying their workers and receiving payments from clients, maintaining cash flow stability.

Healthcare

Healthcare providers often face delays in receiving payments from insurance companies and patients.

Factoring offers a solution by providing immediate cash flow, allowing healthcare providers to cover operating expenses and invest in medical equipment and facilities.

Construction

Construction projects typically involve substantial upfront costs and long payment cycles.

Factoring helps construction companies manage their cash flow by providing advance payments on invoices, enabling them to pay subcontractors and suppliers promptly.

How to choose a factor

When selecting a factoring partner, companies should consider several factors to ensure they choose the right provider for their needs:

- Reputation and experience: look for factors with a good reputation and extensive experience in your industry. Check references and reviews from other businesses to get a better picture of their reliability.

- Fee structure: understand the fees involved in the factoring agreement, including advance fees, discount rates, and any additional service fees. Compare offers from multiple factors to ensure competitive pricing.

- Terms and conditions: carefully review the terms and conditions of the factoring agreement, including recourse vs. non-recourse factoring, advance rates, and payment terms. Ensure the terms align with the business's financial needs and risk tolerance.

- Customer service: choose a factor that provides excellent customer service and is responsive to inquiries and concerns. This is particularly important if the factor will be interacting with the business's customers.

- Technology and reporting: consider factors that offer robust technology platforms and reporting tools, enabling businesses to track their invoices and payments easily.

Factoring provides immediate access to financing

Factoring stands out as a powerful financial solution for businesses grappling with limited access to capital due to tied-up funds in unpaid invoices.

By converting accounts receivable into cash through collaboration with a factoring company, businesses can unlock liquidity, bolster cash flow, and fuel growth initiatives without the constraints of lengthy payment terms.

Key takeaways: Factoring

1. Strategic Financial Advantage (Working Capital)

- Cash Flow Acceleration: Factoring provides immediate liquidity, enabling a business to meet short-term obligations (payroll, supplier payments) without waiting for customer payment cycles.

- Working Capital Optimization: It dramatically reduces the company's Days Sales Outstanding (DSO), thereby shortening the Cash Conversion Cycle (CCC). This means cash is tied up in receivables for less time, allowing faster reinvestment in growth.

- Scalability: Factoring is inherently flexible and scales with sales. As your revenue and invoices increase, the amount of financing available increases automatically, unlike traditional bank loans that require re-negotiation.

2. Risk and Liability

- Recourse vs. Non-Recourse: The most critical decision is who bears the non-payment risk:

- Recourse Factoring: The business retains the risk; if the customer defaults, the business must buy the invoice back. (Lower cost).

- Non-Recourse Factoring: The Factor assumes the credit risk of the customer. (Higher cost, but provides bad debt protection).

- Cost: Factoring is often more expensive than conventional bank debt due to the high risk involved, but the cost must be weighed against the opportunity cost of having capital locked up for months.

3. Operational and Dilution Impact

- Non-Dilutive: Since factoring is the sale of an asset, it does not involve selling equity or giving up ownership, control, or board seats.

- Administrative Relief: In most models, the Factor takes over the administrative burden of collections, dunning, and receivables management, freeing up the business's internal resources.

- Customer Relationship: While less of a stigma today, businesses must carefully select a professional Factor (especially in Open Factoring) to ensure their collection methods align with the business's customer service philosophy.

Summary: Factoring

The factoring transaction is legally an asset sale, not a loan, and involves three core steps:

- Invoice Sale & Initial Advance: The business sells its outstanding invoices to the Factor. The Factor immediately advances a high percentage of the invoice value, typically the Advance Rate (ranging from 70% to 90%), to the seller.

- Collection: The Factor assumes responsibility for collecting the full payment from the customer (the debtor). This is often done openly (Notification Factoring).

- Final Settlement: Once the customer pays the Factor, the Factor remits the remaining balance (the Reserve) to the seller, minus the Factoring Fee (or Discount Rate).

Q&A: factoring

Is Factoring considered 'Debt' or an 'Asset Sale' on the balance sheet?

Factoring is legally classified as an Asset Sale. The Accounts Receivable asset is removed from the balance sheet, replaced by cash.20 This differs from a loan where the Accounts Receivable asset remains, but a corresponding liability (the loan) is added.

What is the risk of using "Selective (Section) Factoring"?

The primary risk is adverse selection. By only factoring receivables from customers who are slow-paying or high-risk, the business signals to the Factor that it is only selling its "bad" assets. This can lead to the Factor requiring much higher fees or declining future services due to a perception of excessive risk.

How does the Factor determine the Advance Rate?

The Advance Rate is determined by the perceived liquidity and creditworthiness of the debtor.21 If the debtor is a large, highly rated, public company, the Factor might offer $\mathbf{90\%}$. If the debtor is a smaller, lesser-known entity, the rate might drop to $\mathbf{70\%}$, reflecting the higher risk that the receivable might not be collected.

Why is Factoring more common in Europe than in the US?

Factoring is a dominant financing method in many European markets due to historical reliance on bank financing, less developed venture debt markets until recently, and the use of government-backed institutions to facilitate trade credit. In the US, the term "asset-based lending" sometimes covers similar concepts but factoring remains the dominant term for direct receivable sales.

Secure your next funding – without giving up equity

Get up to €5M in non-dilutive funding with re:cap. Calculate your funding terms and see how much growth capital you could get.

Calculate funding terms