What is a convertible loan? (and why startups use it)

Raising capital as a startup isn’t always fast or easy. Early-stage startups often need money before they can secure a full equity round.

That’s where a convertible loan comes in.

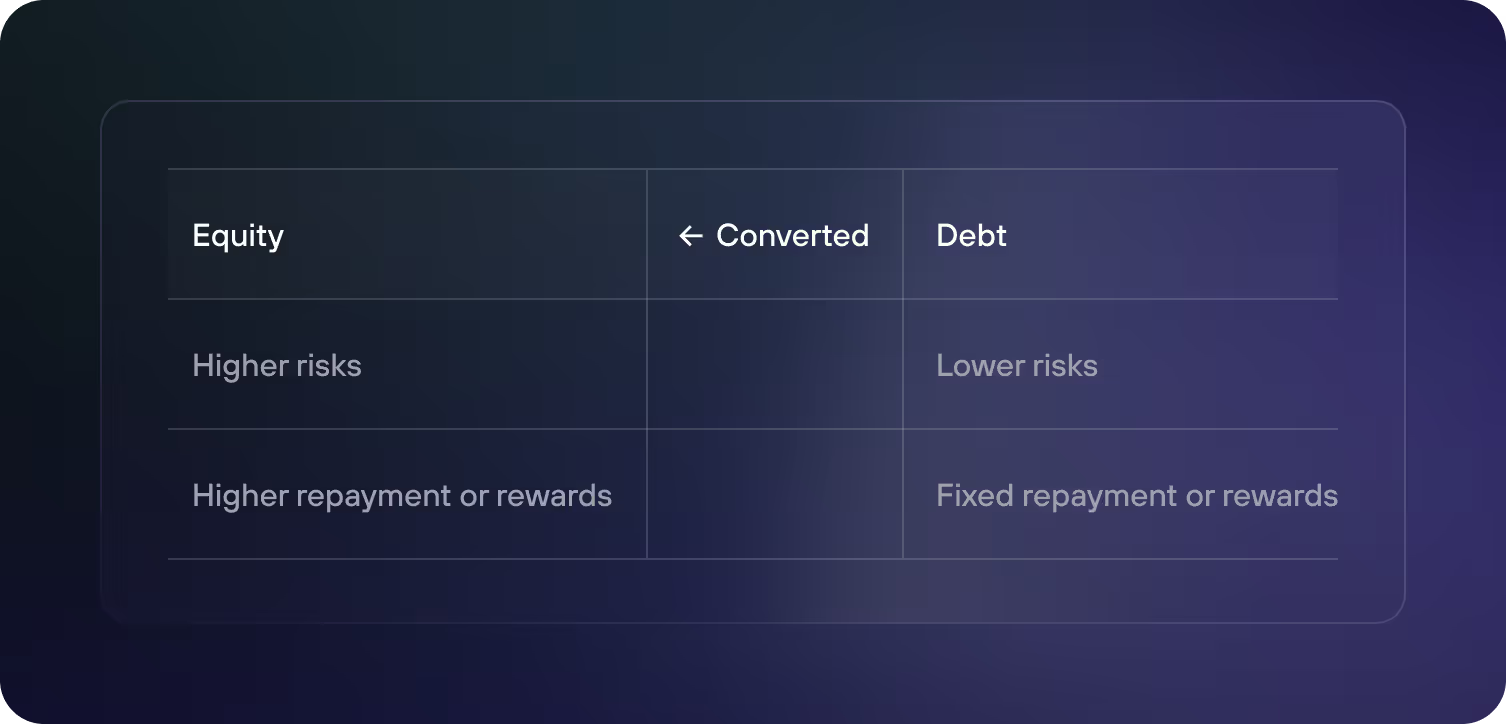

This hybrid financing instrument blends debt and equity. It starts as a loan, but converts into shares later – usually during the next funding round.

Convertible loans (also called convertible notes) are fast, flexible, and often used to bridge gaps between equity rounds. They are financial instruments that offer flexibility and benefits to investors and companies – without valuing the company.

Startups require capital at various stages: when starting their business, for further growth, or between funding rounds. However, securing funding from venture capital is time-consuming and challenging. And it has become much more difficult.

In this guide, you'll learn:

- What a convertible loan is and how it works

- Key advantages and risks for founders

- What terms to watch for in convertible loan agreements

Definition: convertible loan explaind

A convertible loan, also known as a convertible note, is a type of short-term debt that converts into equity, typically in the form of shares, at a later stage, usually during a subsequent financing round.

What triggers the conversion?

- A new equity round (priced round)

- Reaching predefined milestones

- A set date or maturity deadline

Imagine a startup in its early stage. It has minimal to no revenue, not yet achieved product-market fit, and an unproven business model, making its future challenging to evaluate.

Due to these uncertainties, the company's value cannot be precisely determined. Everything depends on positive outlooks for the future. Convincing venture capital fonds and business angels to invest in this situation can be a challenge.

Yet, the startup urgently needs capital. Its cash runway is only a few months. It requires bridging with fresh capital until the next financing round.

Why convertible loans are popular in startups

Early-stage startups often:

- Lack revenue

- Have no product-market fit yet

- Can’t be reliably valued

But they still need cash. A convertible loan solves this by providing liquidity now, with valuation deferred to a later, more stable round.

Key reasons startups use convertible loans

- Faster and cheaper than traditional VC rounds

- No immediate valuation needed

- Delays negotiation on ownership

- Keeps the cap table clean (until conversion)

How does a convertible loan work?

This is where a convertible loan as an alternative financing option comes into play. Convertible loans are loans through which startups receive debt capital – but with a particular feature.

A convertible loan grants lenders the right to convert debt into equity at a later date, typically during the next financing round.

Here's a typical flow:

- Startup raises a convertible loan from early investors

- The investor receives a legal promise of future equity

- When a trigger event occurs (usually the next VC round), the loan converts into shares

Secure your next funding – without giving up equity

Get up to €5M in non-dilutive funding with re:cap. Calculate your funding terms and see how much growth capital you could get.

Calculate funding termsStartups quickly obtain capital, investors reduce their risk

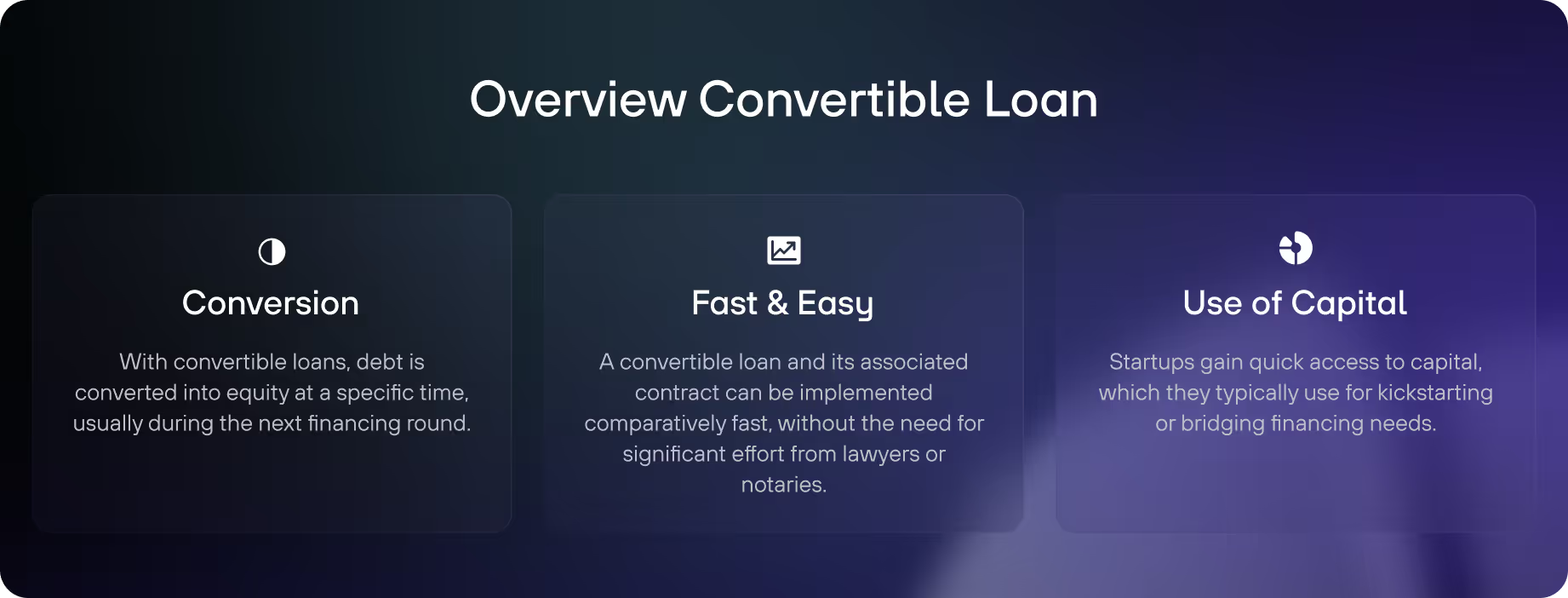

Startups gain rapid access to capital, much faster than with other financing sources. They typically use a convertible loan for:

- Seed funding: To make necessary investments and boost growth.

- Between financing rounds: To extend their runway, enabling them to reach the next round and secure fresh capital.

However, the quick access to capital comes at a certain cost of capital.

Initially, startups take on debt that they theoretically need to repay.

If debt is converted into equity, the investors acquire company shares at a significantly lower price than new investors. This leads to a higher dilution of company shares.

On the other hand, investors with a convertible loan engage in a certain risk mitigation.

In the initial phase, they only provide debt capital with a fixed term, interest, and repayment rates.

The risk is more manageable than with an equity investment. Debt capital can later be converted into equity, depending on whether the conversion was set as a right or obligation in the contract.

Characteristics of convertible loans

A convertible loan is quickly executable

Months of analysis and negotiations with investors about a company's fair valuation? All of this is initially set aside when it comes to convertible loans.

The involved parties require only minimal information to make a decision.

Convertible loans are often an instrument through which existing investors provide additional fresh capital. They are familiar with the startup and have already evaluated it closely during their initial investment.

When founders are in discussions with investors regarding financing, the company valuation plays a crucial role. The value of a share determines how many shares a company must give up (dilution) and the amount that investors will invest in the company.

In the case of convertible loans, this is not foreseen. Company valuation is not part of the negotiations. The involved parties await the next financing round, during which the lenders will base their valuation on the valuation determined at that time.

This speeds up the process and makes convertible loans a relatively quick-to-implement financial instrument.

Contracts are easy to draft

Typically, it only takes two to five pages to draft a convertible loan agreement. In the case of a VC funding, it can involve up to 50 pages. This also positively affects the costs associated with drafting such contracts, as it doesn't require lawyers or notaries.

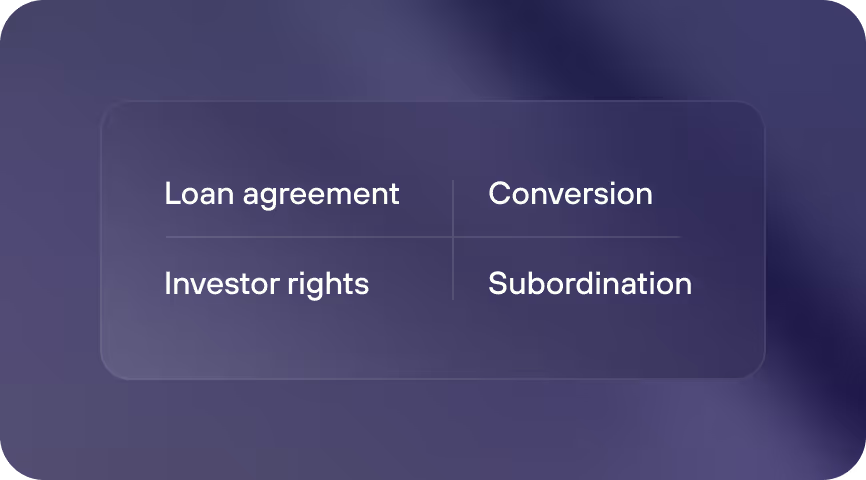

Such a convertible loan agreement includes:

- The loan agreement

- Information about the conversion process

- Investor's rights

- Provisions regarding subordination

In particular, the rules for conversion and investor rights are essential components of this contract. We will delve into each of these components in detail below.

Convertible loans are flexible

Repayment at the end of the term? Interest-free period? Height of the conversion discount? Valuation Cap?

All of these elements can be flexibly tailored to suit the needs of the parties involved. That makes convertible loans relatively flexible. The interests of startups and investors can quickly align.

Smaller financing amounts

The granting of million-euro amounts is rather rare with convertible loans, at least in the early stages of a startup.

Funding amounts typically range from €100,000 to €500,000.

Due to the uncomplicated nature of the contract, startups can also finance themselves with several convertible loans, each for smaller amounts.

However, convertible loans are not only interesting for early-stage companies but also for startups in the growth phase.

Convertible loans are both: debt and equity

A convertible loan is an alternative financing instrument, sitting between debt and equity.

It represents a blend of both and, therefore, it’s characterized as mezzanine capital. Banks treat it as "equity-like", which positively impacts the company's creditworthiness.

The pros and cons of a convertible loan

Pros of convertible loans for companies

- Quick access to capital.

- Flexible and uncomplicated contract structure.

- Low costs associated with contract drafting.

- Interest and repayment typically occur at the end of the term, minimizing the impact on the companies' cash flow.

- The companies credit line increases, as banks view the convertible loan as "equity-like."

- Lenders do not have voting rights in the company until conversion.

Pros of convertible loans for investors

- Flexible and uncomplicated contract structure.

- Investors have the opportunity to convert their loan into equity, allowing them to share in the company's future growth and success.

- If the company fails to meet its growth targets or raise further funding, investors can still claim their principal and interest.

- The conversion discount and valuation cap offer investors additional incentives, as they can acquire shares at a lower price than future investors.

Cons of convertible loans for companies

- Convertible loan lenders offset their risk by receiving a high discount (20 to 30%) on the next company valuation.

- Depending on the contract's structure, a valuation cap can result in capital providers acquiring more shares at an even lower price.

- A convertible loan does not automatically mean that debt capital will convert into equity. If not, the company must repay the loan including interest.

- Convertible loan providers are typically considered silent partners – they rarely contribute their expertise and network to the startup.

Cons of convertible loans for companies

- The future valuation and conversion terms introduce uncertainty regarding the ultimate equity stake.

- If the company fails to achieve a subsequent funding round or predefined milestones, investors may not benefit from conversion.

- Until conversion, investors typically have limited control or influence over company decisions compared to equity shareholders.

What is a convertible loan agreement?

As mentioned earlier, a convertible loan agreement can be drafted relatively quickly. Here are its key components:

Loan agreement

Contains provisions related to loan disbursement, including:

Timing of disbursement

- Is the disbursement made all at once?

- Is the disbursement made in tranches?

- Are there any milestones attached to the disbursement?

Time period

The duration of a convertible loan is rather short- to mid-term, usually ranging from one to three years.

Interest rate

- How high is the interest rate?

- Is there a grace period?

Repayment terms

- How high is the repayment rate?

- Is the repayment rate paid regularly (e.g., monthly) or at the end of the term?

Conversion

Describes the conditions under which debt can be converted into equity or a company shareholding.

Key elements of the conversion include:

- Whether it is a right or obligation for the investors.

- The formula for calculating the shares investors receive.

- Information about the valuation discount and valuation cap.

- A mechanism to secure the conversion, which may involve commitments from the company or the founders or management.

Investor rights

Investor rights outline the rights granted to investors, such as participation in decision-making, access to information, or other privileges like liquidation preferences (distribution of exit proceeds).

Subordination

Convertible loans typically come with a qualified subordination clause. In the event of insolvency, the repayment claim of convertible loan lenders is placed at the very end of the list of creditors ("subordinated"). This is because investor claims are treated as equity, and thus not considered a liability of the company.

Key terms in a convertible loan agreement

The process behind a convertible loan conversion

Several steps precede the conversion of debt to equity. These include:

Shareholder resolution to conclude a convertible loan agreement

To enter into a convertible loan agreement, a shareholder resolution is required. This typically requires a simple majority in the shareholders' meeting, usually composed of the founders (in the case of a startup).

Execution of the convertible loan agreement

With the approval of the shareholders' meeting, the convertible loan agreement can be executed.

The startup receives capital, and the loan becomes effective. Companies can find a standard contract for this at the German Startups Association.

Capital increase resolution

At the end of the contract term, investors have the right or obligation to convert their loans into company shares.

A capital increase is necessary because the company must issue additional shares. Within the shareholders' meeting, this resolution requires a 75% approval.

Final conversion

After the capital increase, the former investors become shareholders of the startup.

This is when the calculations for the valuation discount or valuation cap come into play. But what are the mechanisms behind those terms?

Valuation discount and valuation cap: differences and calculation

The valuation discount determines the discount that investors receive on the shares.

This means that they pay less per share than new investors. The discount usually ranges between 20 to 30%.

The valuation cap is the maximum company valuation at which debt capital converts into equity.

For example, if the convertible loan providers set the Valuation Cap at €5 million, but the startup is valued at €10 million in the next financing round, the convertible loan providers will convert at the predetermined valuation of €5 million.

However, the valuation discount and Valuation Cap typically do not apply together.

The parties contractually agree in advance that the convertible loan providers must choose one of the two instruments at the time of conversion.

Calculation of a convertible loan with a valuation discount

Initial situation: A startup founder holds all 100,000 company shares.

An investor enters with a convertible loan

- The investor offers funding through a convertible loan of €100,000.

- The loan includes 8% interest with a one-year term.

- Repayment and interest are due at the end of the term.

- The convertible loan has a 20% valuation discount, applicable during the next financing round.

- There is no valuation cap.

A new VC funding round occurs one year later

- A venture capital fund enters with €500,000.

- The company valuation is €5 million.

- €5 million / 100,000 company shares = €50 per share.

- €500,000 / €50 per share = The VC acquires 10,000 shares.

Simultaneously, the convertible loan takes effect.

- €100,000 repayment + €8,000 interest = €108,000 debt capital.

- €50 per share – 20% valuation discount = €40 per share for the convertible loan provider.

- €40 per share – €1 nominal value per share during the capital increase = €39 per share as conversion price.

- €108,000 / €39 per share = 2,769 shares for the convertible loan provider.

Example calculation of a convertible loan with a valuation cap

Initial situation: A startup founder holds all 100,000 company shares.

An investor enters with a convertible loan

- The investor offers financing through a convertible loan of €100,000.

- The loan includes 8% interest with a one-year term.

- Repayment and interest are due at the end of the term.

- The convertible loan is set with a Valuation Cap of €3 million.

- There is no discount on the valuation.

A new VC funding round occurs one year later

- A venture capital fund enters with €500,000.

- The company valuation is €5 million.

- €5 million / 100,000 company shares = €50 per share.

- €500,000 / €50 per share = The VC acquires 10,000 shares.

Simultaneously, the convertible loan takes effect.

- €100,000 repayment + €8,000 interest = €108,000 debt capital.

- €3 million Valuation Cap / €5 million company valuation = 0.6 valuation cap.

- €50 per share * 0.6 valuation cap = €30 per share for the convertible loan provider.

- €30 per share – €1 nominal value per share during the capital increase = €29 per share.

- €108,000 / €29 per share = 3,724 shares for the convertible loan provider.

In this scenario, the valuation cap can serve as an incentive for investors to participate in a startup as early as possible and take on the additional risk.

Convertible loans are a dynamic financing instrument

Convertible loans offer a valuable financing solution for startups facing challenges in securing traditional VC funding.

By transforming debt into equity, these loans provide rapid access to capital without the need for precise company valuations, making them particularly attractive for early-stage businesses.

Key aspects of convertible loans include their flexibility, quick execution, and relatively straightforward contract structures.

They allow startups to bridge financing gaps between funding rounds and fuel their growth without the complexities associated with traditional equity investments.

However, while convertible loans offer benefits such as quick access to capital and low costs associated with contract drafting, they also come with potential drawbacks.

These include the dilution of company shares and the risk of high discounts on future valuations for investors.

Overall, convertible loans represent a hybrid financing instrument that balances the interests of startups and investors, providing a valuable alternative to traditional funding methods.

Summary: convertible loans

A convertible loan quickly transforms debt into equity, giving startups fast access to capital without needing an immediate company valuation.

It’s a flexible, cost-effective alternative to venture capital funding, particularly useful in early stages or between financing rounds.

Startups benefit from quick funding, while investors mitigate risk by starting with debt rather than equity.

However, high discounts can dilute shares, and if the loan doesn’t convert, it must be repaid. Despite these challenges, convertible loans remain a smart choice for rapid, flexible financing.

Secure your next funding – without giving up equity

Get up to €5M in non-dilutive funding with re:cap. Calculate your funding terms and see how much growth capital you could get.

Calculate funding terms