Revenue-based financing (RBF) is non-dilutive growth funding.

You get capital upfront. You repay it as a percentage of your revenue until you hit a repayment cap.

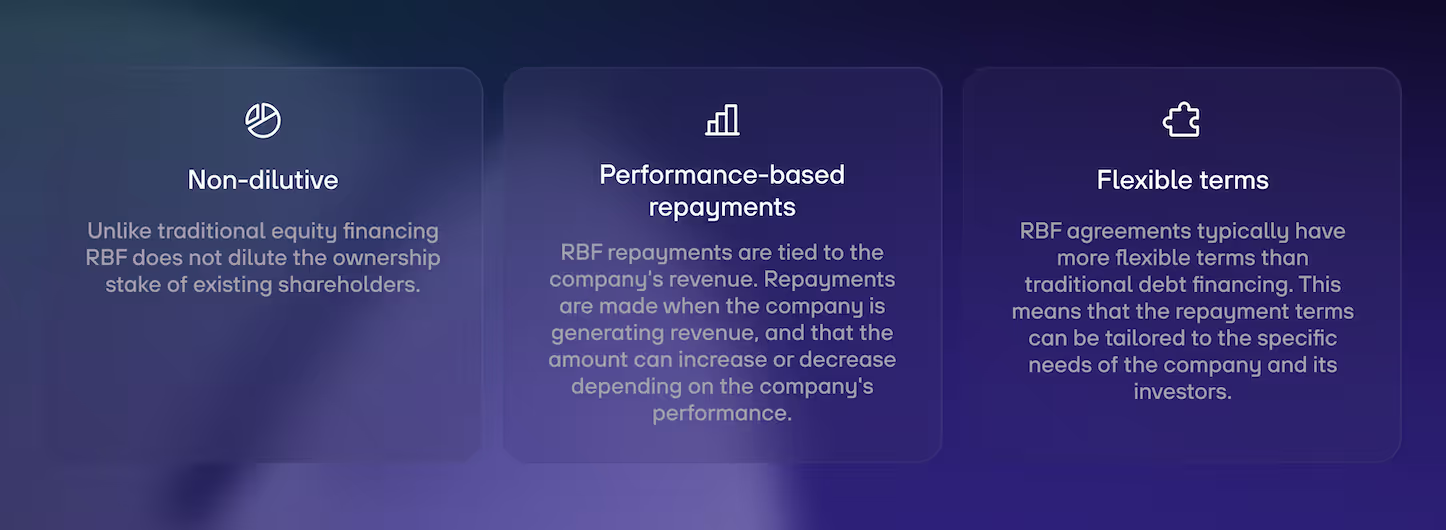

No equity. No board seat. No fixed monthly installment.

That makes RBF attractive if you want to grow fast, without giving away ownership or taking on rigid debt payments.

Also known as revenue-based loans, revenue share financing, or revenue-based funding, this alternative financing instrument is increasingly popular among SaaS startups and subscription-based businesses with predictable income streams.

RBF is already well-established in the U.S. and U.K., and it’s gaining traction in Germany and across Europe. With the global market expected to surpass $9.8 billion in 2025, revenue-based financing has become an option for startup funding and high-growth companies.

What you'll learn in this guide

- How RBF works (in plain English)

- Typical RBF terms (and what they really mean)

- The real cost of RBF (and when it gets expensive)

- When RBF is a good idea, and when it isn’t

- Alternatives you should compare before signing

Revenue-based financing: Definition

Revenue-based financing is a funding model where investors provide capital in exchange for a fixed share of your future revenue until a pre-agreed total repayment is reached.

Think of it as: Capital now → repay from revenue later → stop when the cap is hit.

It’s debt-like (you have to repay), but payments are performance-linked instead of fixed.

RBF provides an alternative or complementary option to equity financing. It adds another layer to a company's capital structure.

How does revenue-based financing work?

An RBF agreement has three core building blocks:

- Funding amount: How much capital you receive.

- Revenue share (royalty rate): The percentage of revenue you pay every month (often 5%–15%).

- Repayment cap (multiple): The total amount you’ll repay (often 1.5×–3× the funding amount).

What happens each month?

- You report your revenue (per the contract definition)

- You pay the agreed percentage

- Payments stop once the repayment cap is reached

If revenue grows, you repay faster. If revenue drops, payments drop too.

Fuel you growth – without giving up equity

Get up to €5M in non-dilutive funding with re:cap. Calculate your funding terms and see how much growth capital you could get.

Calculate your funding termsExample for revenue-based financing for companies

The conditions:

- A company generates monthly recurring revenue (MRR) of €500,000 at the beginning of the financing.

- Now, it is in touch with an RBF investor and wants to raise €500,000.

- The company agrees with the RBF investor on a monthly revenue share of 10%.

- The cap of the repayment amount is at a maximum of €1,000,000.

Due to the steady revenue growth, the company has repaid its financing to the investor after 12 months. Revenue growth is the only criterion that determines the margin of repayment. Why?

Investors thoroughly assess a company’s financials

With revenue based financing, there are no classic repayment or interest rates. It is based only on revenue growth.

Thus, for investors it is essential to conduct a data-based analysis of the company's financial metrics.

Since the return on investment expected by investors is tied to future revenues, this assessment has to be in-depth and solid.

Investors treat revenue and the customer base as assets that need to be valued. They focus on asset-light businesses within the tech and platform environment.

For the assessment, the investor analyzes different financial KPIs. The basis is revenue, customer base, cash flow, and bank data. These KPIs are pivotal in determining the investment decision, the amount of financing, and its percentage share of revenue.

Among those metrics are:

- Monthly and annual revenue growth (MRR/ARR)

- Customer Churn Rate

- Customer Concentration

- Net Dollar Retention (NDR)

These financial metrics allow investors a better analysis of companies with recurring revenues, which are likely from the SaaS or software industry. They can make better-informed predictions about the revenue development of those companies.

Therefore, startups considering revenue-based financing should have relevant and up-to-date data available before raising capital.

RBF term sheet: the clauses that decide what you really pay

Most founders compare RBF offers by “percentage + cap”. Two contracts can show the same headline terms, and behave completely differently. Here are the clauses you should understand (and negotiate).

1. "Revenue" definition (this is the big one)

What counts as revenue for repayment?

Common questions:

- Gross revenue or net revenue?

- Are refunds and chargebacks excluded?

- Are taxes excluded?

- What about reseller / marketplace revenue?

- What about one-time services, hardware, usage fees, FX effects?

If the revenue definition is too broad, you’ll pay more than you expect.

2. Revenue share percentage

The contract should clearly state:

- The percentage

- The reporting period (monthly/weekly)

- Whether there’s a “true-up” if revenue numbers change later

3. Repayment cap / multiple

This is the total you repay.

But you should also ask:

- Does the cap include fees?

- Are there “final payments” at maturity?

- What happens if you haven’t hit the cap by the end date?

4. Fees (often overlooked)

Possible fees include:

- Origination / setup fee

- Servicing fee

- Platform fee

- Legal fees

Fees can quietly push your effective cost up.

5. Minimum payments (or minimum revenue assumptions)

Some deals include:

- A minimum monthly payment

- A minimum revenue baseline

- A "catch-up" mechanism

That can turn "flexible repayment" into "almost-fixed repayment."

6. Term length and maturity

Some RBF deals have a maturity date.

If you haven’t repaid by then, the contract may trigger:

- A balloon payment

- A refinancing requirement

- Penalty pricing

7. Reporting + audit rights

Standard is periodic reporting.

But watch for:

- Overly frequent reporting requirements

- Broad audit rights

- Strict penalties for late reporting

8. Default triggers

Look for:

- Missed payments

- Reporting delays

- Changes in control

- Breach of covenant-like obligations

Default language drives risk. Even if you "expect to pay".

9. Prepayment terms

Can you repay early?

If yes:

- Is there a discount?

- Is there a penalty?

- Are you still paying the full cap?

This matters if you plan to raise equity later or exit early.

What does RBF really cost?

RBF doesn’t look like an interest rate. But it still has a cost of capital. Here’s how to think about it without finance jargon:

The faster you grow, the more expensive it gets

If revenue grows quickly:

- Payments grow quickly

- Investors get repaid faster

- The implied return rises

That’s why RBF can feel "fine" at moderate growth, and "surprisingly expensive" at high growth.

A practical way to compare offers

When you compare RBF offers, always model:

- How long repayment takes at realistic growth

- Total repayment (cap + fees)

- Cash impact on runway and reinvestment

If you want a single number, ask providers for an implied IRR under different growth scenarios. Then validate it yourself.

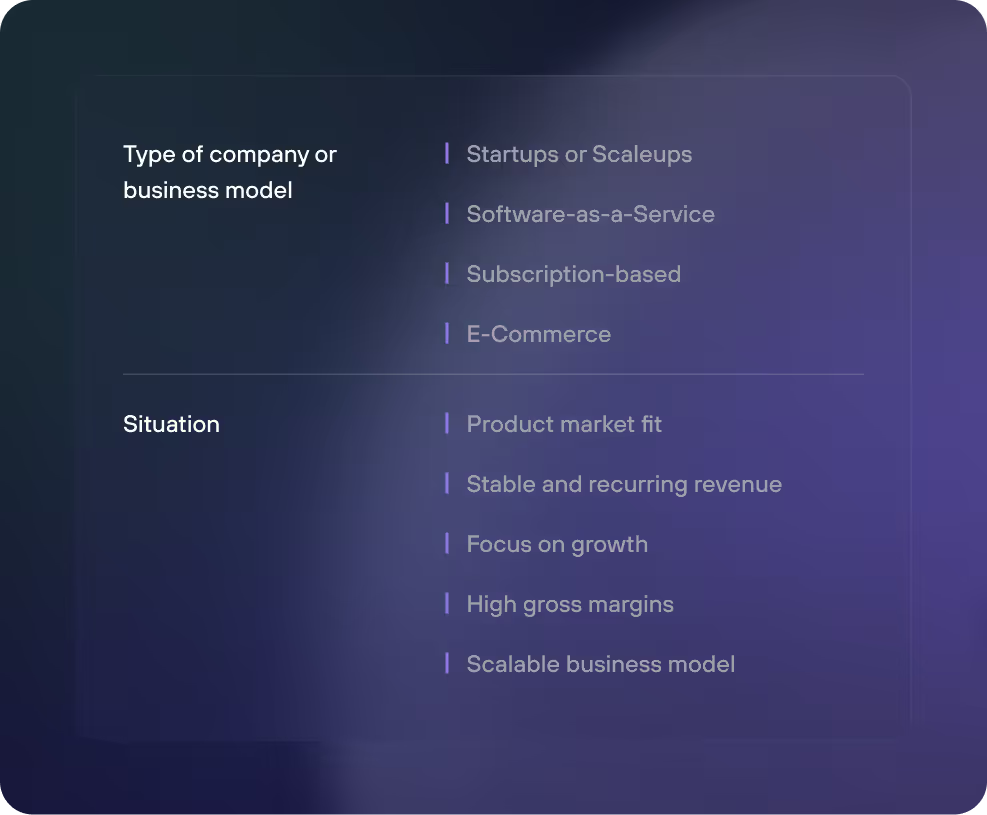

Who qualifies for revenue-based financing?

Not every company is a fit for revenue-based financing (RBF).

To secure funding, you’ll need to prove that your business generates stable, recurring revenue and has the margins to sustain repayments.

Common eligibility benchmarks

- Monthly Recurring Revenue (MRR): Typically €30,000 or more

- Annual Recurring Revenue (ARR): €300,000 to €1M+

- Gross Margin: Ideally 60% or higher

- Churn: Low and improving

- Retention: Net Dollar Retention (NDR) above 100% is a plus

Why this matters: RBF investors don’t get equity or interest. They’re paid out of future revenue. So your predictability and margin profile directly influence how much you can raise and on what terms.

Ideal candidates for RBF are SaaS, subscription commerce, and platform businesses with strong customer retention and reliable MRR.

Until startups have met these three conditions, debt funding – and thus RBF – rarely makes sense or is a good option.

When RBF is a good idea

RBF works best when you already have a growth engine, and want to pour fuel on it.

Good use cases

- Fund marketing and sales ramp (when CAC payback is proven)

- Bridge to a higher valuation round

- Smooth working capital in a subscription model

- Finance expansion without board complexity

What it won’t solve

RBF will not fix:

- weak product-market fit

- unclear unit economics

- structural burn with no path to profitability

- poor revenue visibility

RBF rewards what’s working. It punishes what’s unstable.

Revenue financing is an alternative to traditional debt

For business owners and startups, the only way to get capital was to sell shares in exchange for equity – with all the negative consequences attached to it:

- In the event of an exit or IPO, investors receive part of the profits.

- Due to the dilution, new shareholders receive co-determination, voting, and control rights over the company. The founders lose influence on decisions and the direction of their own company.

- VC financing ties up the company's resources (due diligence) and the founder's time (negotiations). It incurs legal and consulting costs, and months can pass before money is in the bank account.

Revenue-based funding enables startups and scaleups to raise debt on an alternative path trough venture lending – without diluting shares and assigning new seats at the table.

Revenue-Based Financing vs. Debt vs. Equity

Here’s the clean comparison most founders need.

Recurring revenue financing and revenue-based financing

Another form of revenue financing is recurring revenue financing (RRF). It is also suitable for startups and early-stage companies focussing on growth.

With RRF, companies raise debt. The financing amount and interest rate are based on the level of recurring revenues. The use cases of RBF and RRF are overlapping, only the repayment terms differ.

RRF means fixed costs in advance

The difference: The costs of RRF are fixed at the beginning of a contract and remain throughout the entire period. They are not attached to revenue growth.

Debt is usually only allocated up to a financing limit, which depends on the annual recurring revenue of a company.

Revenue-based financing is for early-stage companies

For companies with constant and recurring revenues, revenue-based financing is a good option and an ideal complement to a traditional loan (debt financing), venture capital (equity financing), or venture debt.

The company is dedicated to its performance and lets investors participate in future revenue growth but without giving up control over its company.

Both sides, investors and companies, pursue the same goal: steady revenue growth. It helps the investors, who get a faster return on their investment, and the company, which increases its value.

For startups, this flexibility means that capital costs adapt to their growth. If future revenues don't develop as expected, repayment and fixed interest rates do not become a permanent burden.

Summary: Revenue-based financing

Revenue-based financing (RBF) is a non-dilutive funding method where companies raise capital by pledging a percentage of future revenues to investors.

Ideal for startups with recurring revenues (like SaaS businesses), RBF offers flexible repayment tied to performance, allowing companies to maintain control without selling equity.

However, RBF has challenges.

Companies need predictable revenues to attract investors, and rapid growth can increase costs due to a higher internal rate of return.

Additionally, receiving funds upfront may lead to overfunding if not immediately utilized. Despite this, RBF is a flexible alternative to traditional loans or equity financing.

Fuel you growth – without giving up equity

Get up to €5M in non-dilutive funding with re:cap. Calculate your funding terms and see how much growth capital you could get.

Calculate your funding terms