Month-end closing is the accounting process of finalizing your company’s financial records at the end of each month.

It means reconciling accounts, reviewing revenues and expenses, booking accruals, and making sure everything adds up before the next reporting cycle begins.

In short: it’s where finance turns chaos into clarity.

This guide exists because closing the books is often harder than it needs to be.

Too many teams still rely on outdated checklists, scattered data, and last-minute scrambles. But a well-run month-end close can become a powerful habit. Founders get real visibility, finance leads control, and accountants peace of mind.

What you'll learn

- What is month-end closing, and what makes a good close process

- How roles like the bookkeeper, controller, and CFO fit together when it comes to book-closing

- How to build month-end closing habits that save time without sacrificing accuracy

TL;DR

- Month-end closing is the process of reviewing, reconciling, and finalizing financial data to ensure the books are accurate and complete.

- A strong close improves reporting, reduces risk, and gives founders and finance teams real visibility into the business.

- Modern teams rely on automation, clear roles, and consistent workflows to make the process faster, cleaner, and more reliable.

Definition: what is month-end closing?

Month-end closing is the accounting process of reviewing, verifying, and finalizing a company’s financial data at the end of each month. It ensures the books reflect reality. It helps teams to report accurately, spot risks early, and make informed decisions.

The month-end close marks the official cutoff for accounting and ensures that every transaction, invoice, expense, and payment, is reviewed, recorded, and reconciled. Once that’s done, the books are closed, and the next month begins with a clean slate.

Key components of month-end closing: Accuracy and accountability

At its core, the month-end close is about accuracy and accountability.

It creates a consistent financial rhythm, helping teams catch errors early, track progress toward goals, and base decisions on up-to-date data. It also lays the foundation for reliable financial statements, tax filings, and investor reports.

Closing the books gives you confidence in your numbers. It shows where the business stands, what’s coming in, what’s going out, and what needs attention.

What’s the timeline of the month-end closing process?

The closing process typically starts on the last day of the month and wraps up within the first few business days of the new month. Some companies close in three days, others take ten or more. The speed depends on headcount, tools, and how well workflows are defined.

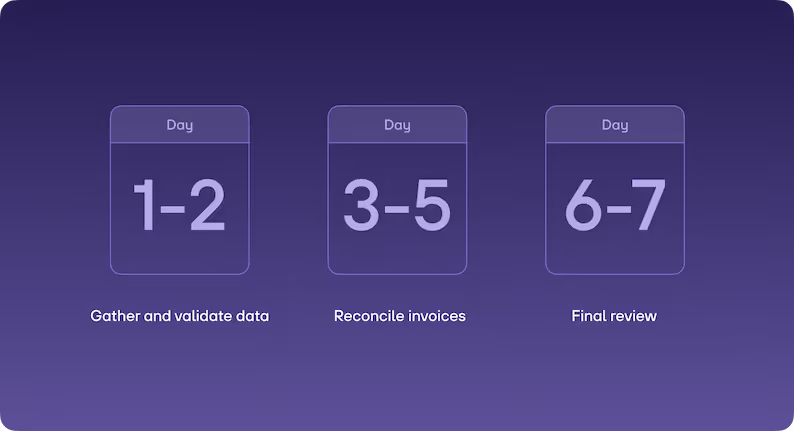

A standard timeline for month-end closing looks like this:

- Day 1-2: gather and validate data from banks, payroll, invoicing tools, and spending platforms.

- Day 3-5: reconcile invoices, book missing entries, check for anomalies.

- Day 6-7: final review, internal approvals, and reporting to leadership or investors.

You want to achieve consistency: same steps, same order, every month. That’s what builds trust in the numbers.

Why is the month-end closing process important?

Month-end closing brings order to your finances. It’s how companies turn a messy pile of transactions into a clear, accurate picture of where they stand.

Without it, decisions are based on guesswork. Numbers lose their meaning. Surprises show up where they shouldn’t.

A proper close ensures that every expense is booked, every invoice is tracked, and every account is reconciled.

It creates a single source of truth the entire company can rely on. Founders see their runway. Finance leads can catch issues early. Investors get clean, timely reports.

It also builds discipline. Teams that close their books regularly are better prepared for audits, board meetings, and funding rounds. They spend less time cleaning up the past and more time with financial plannings for the future.

What are key activities in month-end closing?

A smooth month-end close is about coordination between teams, systems, and deadlines. Core activities include:

- Bank reconciliations: match bank statements with your books to ensure an accurrat cash position.

- Revenue and expense review: confirm all invoices and bills are recorded in the correct period.

Accruals and deferrals: account for revenue earned or costs incurred that haven’t hit the books yet. - Payroll checks: ensure salaries, bonuses, and taxes are posted correctly.

- Journal entries: post manual adjustments where automation falls short.

- Internal reviews: controllers or CFOs sign off before reports are shared.

Dependencies matter with month-end closing. If HR delays payroll exports or the sales team forgets to submit invoices, closing stalls. That’s why communication and clean data flows are as important as accounting know-how.

Let your books close themselves

Enjoy clean books: streamline your accounting process and turn invoice reconciliation from days into minutes.

Start 14-day free trial7 Steps: how a month-end close is done

Month-end closing is a method.

The process follows a series of well-defined steps that bring financial clarity to the business. Speed and accuracy depend on structure, discipline, and clean data. Here's how it typically works:

1. Collect all financial data

Start by gathering the raw materials: bank statements, credit card reports, invoices, bills, payroll summaries, and data from your ERP or accounting system. Missing inputs here will stall the entire close.

2. Reconcile accounts

Start with pre-accounting: check that internal records match external sources. This includes:

- Bank and credit card reconciliations

- Accounts receivable and payable balances

- Intercompany transactions, if applicable

3. Post accruals and adjustments

Not all transactions arrive neatly by month’s end. That’s where accruals and deferrals come in. Book revenue earned but not yet invoiced. Record expenses incurred but not yet billed. Make manual journal entries where needed.

4. Review the general ledger

Scrub the ledger for errors, duplicates, or odd spikes. Investigate discrepancies. Confirm account classifications. This is the moment to catch mistakes before they snowball into bigger problems.

5. Prepare internal reports

Summarize financial performance with clean, up-to-date numbers. Common reports include:

- Profit and loss (P&L) statement

- Balance sheet

- Cash flow statement

- Department or project-level breakdowns

These reports feed leadership, investors, and tax authorities. They also guide internal decisions.

6. Approve and close

Once reviewed and confirmed, the period is closed in the accounting system. No further edits are allowed. You’re now ready to roll into the next month.

A smooth close depends on repeatable processes and clear ownership. Everyone needs to know what they’re responsible for and by when. With the right setup, month-end closing becomes less of a grind and more of a habit. The kind that drives better business decisions.

7. Information needed by accounting to close the monthly books

To close the books accurately and on time, accounting teams need a full picture of the company’s financial activity for the month. Data needs to be complete, timely, and correct. Without it, the monthly closing slows down or breaks entirely.

Here’s what accounting depends on:

The month-end workflow

Closing the books used to mean one thing: long hours, dozens of Excel files, and a flurry of emails to answer basic questions. Today, that’s no longer the only way. The month-end workflow has changed. For teams willing to modernize, it’s become faster, cleaner, and more collaborative.

Traditional workflows were built for accountants, not teams

In a classic setup, the month-end close followed a rigid, mostly manual sequence:

- Bank reconciliations

- Invoice matching

- Journal entries

- Trial balances

Each step was siloed, often delayed by missing data or miscommunications. Collaboration meant walking over to someone’s desk. Transparency was an afterthought.

Worse, the process didn’t scale. As a company grew, the complexity multiplied: more transactions, more stakeholders, more friction. It was risky. Errors crept in. Insights came too late. And the finance team became the bottleneck instead of the enabler.

Month-end closing is a team sport

Today’s best workflows look very different. They rely on real-time data, not static spreadsheets.

Tasks are tracked in project management tools, not someone's head. Teams work together in shared dashboards. And automation takes care of the grunt work. It pulls bank feeds, categorizing expenses, and flagging inconsistencies.

This shift is about control:

- Finance leaders can now see exactly where the close stands, who’s responsible for what, and what’s blocking progress.

- Founders can get early visibility without waiting for final numbers.

- Accountants can focus on judgment calls instead of copy-pasting data.

Automation handles the routine, humans handle the nuance

Software helps to eliminate repetitive tasks. The real value lies in how it supports collaboration. When everyone works from the same source of truth, whether it’s a live accounting system or a shared closing checklist, mistakes drop and trust rises.

The result? A month-end close that’s not only faster, but more accurate, more transparent, and a lot less painful.

What are key roles and responsibilities in the month-end closing process?

A smooth month-end close depends on clear roles. When everyone knows what they’re responsible for, the process runs faster, cleaner, and with fewer surprises. Whether the team is in-house, outsourced, or a mix of both, knowing who does what is non-negotiable.

In-house vs. external: ownership is key

Some companies keep all roles internal. Others outsource parts of the close, especially bookkeeping and controlling. Both setups can work, but clarity matters.

Someone inside the company must still own the process. You can’t outsource responsibility. Whether it’s the finance lead or the CFO, someone needs to keep the timeline tight, the tools in sync and the team aligned.

What matters most isn’t who carries the title but every task has a name next to it. That’s how you avoid dropped balls, missed deadlines, and last-minute fire drills. Clear roles build trust. And trust is what keeps the close moving.

Best practices for smoother month-end closing

The close doesn’t have to be a scramble. With the right habits and tools, it can become a steady rhythm. These best practices save time, and raise the quality of your numbers and the confidence behind your decisions.

1. Automate what doesn’t need a human

Every minute spent copying data between systems is a minute wasted. Use tools that sync bank feeds, pull invoices automatically, and match payments to transactions. Automation reduces errors, speeds up repetitive tasks. It frees up the team to focus on judgment, not data entry.

2. Reconcile early and often

Don’t wait until the last day of the month to reconcile accounts. The closer you get to real-time reconciliation, the less cleanup you’ll face at the close. Bank balances, credit cards, payroll entries: keep them aligned as you go. It’s faster in the long run, and it gives you better visibility throughout the month.

3. Keep a clean audit trail

Every adjustment should be traceable. Every document should be easy to find. Whether you're preparing for an audit or just explaining last quarter’s jump in software costs, good documentation pays off. Use tools that track changes and attach supporting files directly to entries. Your future self, and your auditor, will thank you.

4. Set realistic timelines

A fast close is great. A reliable one is better. Don’t chase speed at the expense of accuracy. Define a close calendar that fits your business and stick to it. Be honest about dependencies: when payroll runs, statements arrive, approvals happen. Then work backwards from there. Consistency builds confidence.

The best finance teams build smart systems, refine their process, and improve month by month. That’s how a painful close becomes a manageable one, and eventually, a competitive edge.

Do you want to see how it's done in the real-world? Read the 9x case study, to see how they automated 90% of their pre-accounting process and saved 8 hours each month.

Summary: Month-end closing

Month-end closing is the backbone of a company’s financial hygiene.

It’s the structured process of reviewing, reconciling, and finalizing all financial activity from the past month. Done well, it creates clarity, reduces risk, and builds trust in the numbers.

Done poorly, it leads to delays, guesswork, and missed opportunities.

Q&A: Month-end closing

What is the difference between month-end closing and year-end closing?

Month-end closing happens every month and focuses on short-term accuracy and reporting.

Year-end closing is a more extensive process that wraps up the entire fiscal year. It includes all month-end steps, plus additional tasks like inventory valuation, tax adjustments, depreciation, annual reporting, and audit preparation.

Month-end closing keeps the business on track while year-end closing prepares it for taxes, investors, and regulatory compliance.

How long should a month-end close take?

For small companies with simple financials, a well-organized close can take 1-2 business days. Mid-sized companies typically need 3-5 days. Larger enterprises with multiple entities or complex operations may need a week or more.

The timeline depends on transaction volume, system integration, and team efficiency. Companies with heavy automation and continuous reconciliation can close in as little as 1 day.

What happens if we miss a transaction during month-end close?

If you discover a missed transaction after closing the period, you'll typically need to book it in the current open period with proper documentation. For material errors that would significantly impact prior period reporting, you may need to reopen the closed period or record an adjusting entry with clear notes explaining the correction. The approach depends on the transaction's size, your company's materiality threshold, and whether you're under audit.

Can you close the books before the month actually ends?

No. You cannot finalize the close until all transactions for the period are complete. However, you can prepare extensively. Many finance teams run "soft closes" a few days before month-end by reconciling through day 25 or 28, reviewing preliminary numbers, and preparing draft reports.

What's the biggest mistake companies make during month-end closing?

Waiting until the last minute to start. The most common failure pattern is treating the close as a single event rather than an ongoing discipline. Teams that reconcile accounts throughout the month, maintain clean documentation as they go, and communicate early about unusual items consistently outperform those who scramble at month-end. The second biggest mistake is skipping reconciliations to save time. This always backfires because errors compound and become harder to trace.

How do you handle month-end closing when key team members are unavailable?

Document everything and cross-train your team. Every critical task should have clear written procedures and at least one backup person who can execute it. Use shared checklists in your project management system so anyone can see task status and ownership. For planned absences, front-load work before the person leaves or adjust the close calendar. For unexpected absences, this is where your documentation and system access controls become critical.

What financial reports are required at month-end close?

At minimum, you need three core financial statements:

- The profit and loss statement (income statement)

- Balance sheet

- Cash flow statement

Many companies also produce departmental P&Ls, variance reports comparing actuals to budget, aged receivables and payables reports, and cash runway projections.

The specific reports depend on your stakeholders: investors may want burn rate metrics, lenders need covenant compliance reports, and department heads want their own cost center breakdowns. Define your required report package early so you're not scrambling to produce ad-hoc requests each month.

How does month-end closing differ between cash basis and accrual accounting?

Cash basis closing is simpler: you're just confirming that recorded transactions match bank activity.

Accrual accounting requires additional steps like booking unpaid invoices, recording expenses incurred but not yet billed, recognizing deferred revenue, and adjusting prepaid expenses.

Accrual closing takes longer but provides a more accurate picture of financial performance because it matches revenue with the expenses that generated it. Most companies beyond the earliest stages use accrual accounting, and it's required for audited financial statements and generally accepted accounting principles (GAAP) compliance.

Let your books close themselves

Enjoy clean books: streamline your accounting process and turn invoice reconciliation from days into minutes.

Start 14-day free trial.png)