Liquidity is no coincidence. It requires a strategy. That’s why you shouldn’t focus your company solely on revenue growth.

Doing so risks financial bottlenecks, even with a full order book. Liquidity management ensures that sufficient funds are always available. This way, you can cover liabilities and seize growth opportunities.

Liquidity management means more than just solvency. You control your liquidity and optimize capital allocation. You reduce financing costs and protect yourself against unexpected risks.

In this article, you’ll learn about the methods and tools companies use to achieve this.

What you’ll learn in this article

- How liquidity management ensures solvency

- How to optimize capital efficiency with liquidity management

- The role of risk management and liquidity planning

TL;DR

- Liquidity management balances security and flexibility – ensuring you can pay obligations while keeping capital available for growth opportunities.

- Follow a systematic 7-step process – from assessing current position to continuous monitoring and optimization.

- Software tools transform liquidity control – real-time insights, automated forecasting, and scenario planning help you stay ahead of cash flow challenges.

Definition: Liquidity management

Liquidity management is the art of managing a company’s cash flow to ensure it remains solvent at all times. It’s not just about having enough cash on hand. Rather, strategic liquidity control is key.

Your company must be able to pay invoices on time without holding excessively high capital reserves that could be profitably used elsewhere. Good liquidity management ensures financial stability. It enables growth and protects against shortages.

Liquidity management creates balance

In short, liquidity management means finding the balance between security and flexibility. Too much tied-up capital slows down investments. Too little liquidity can be dangerous and can lead to insolvency.

To avoid this, there are various methods and tools: from cash flow planning to flexible credit lines (such as those offered by re:cap) to software solutions for liquidity control and planning (also offered by re:cap).

Especially in economically uncertain times, it’s crucial to keep track of your liquidity. This keeps you flexible and allows you to mitigate financial risks in time.

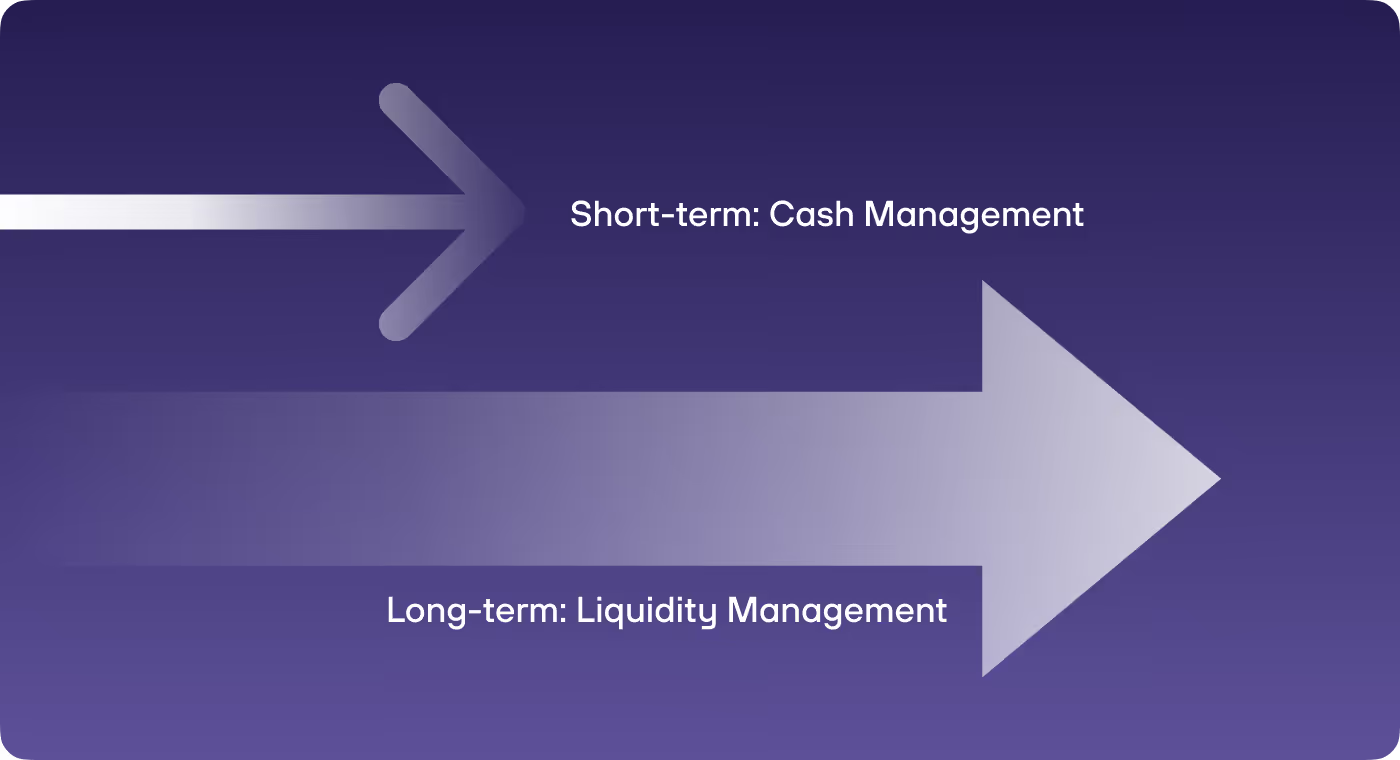

Cash Management vs. Liquidity Management

Liquidity management and cash management are related but not identical concepts. They are used differently in a business context:

Cash Management

Cash management is more operational and focuses on the short-term control of a company’s cash flow. This includes:

- Account and transaction overview

- Cash flow analysis

- Daily payment transactions

- Cash pooling

The goal is to efficiently manage daily transactions and ensure that the company remains solvent at all times.

Liquidity Management

Liquidity management is more strategic and includes medium- and long-term liquidity planning in addition to short-term cash management. This involves:

- Liquidity forecasts

- Managing liquidity reserves

- Evaluating different financing options

- Optimizing working capital

The goal is to manage your company’s finances in the long term while balancing stability and flexibility.

Cash management ensures daily liquidity. Liquidity management shapes a company’s overall liquidity strategy. Let’s take a look at the tasks and functions involved.

Manage, forecast, and secure liquidity

Use re:cap to manage your liquidity. Track your cash flow in real time, forecast it, and fill short-term cash gaps with debt funding from re:cap.

Start 14-day free trialTasks and functions of liquidity management

Liquidity management deals with the broader financial management of your company. It fulfills key functions and tasks that are crucial for business success.

Fundamentally, you need an overview of two things: your current liquidity and your future liquidity. Based on this, various tasks and functions arise, including:

Let’s examine each of these areas in more detail.

Ensuring solvency

One of the main tasks is ensuring solvency because even the best business model is worthless if you can’t pay your invoices or salaries.

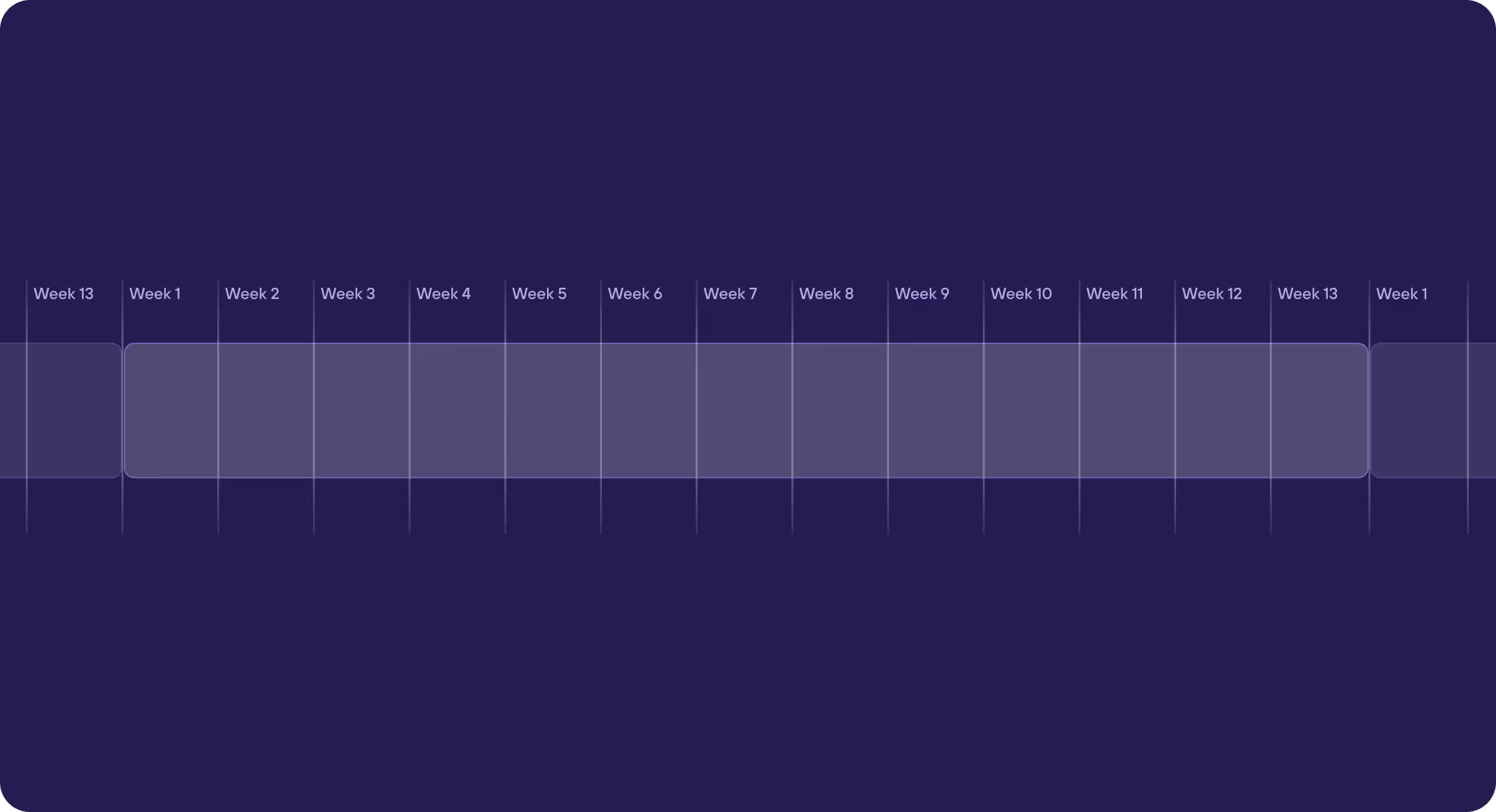

Liquidity planning and scenario analysis

Another important task is liquidity planning. You need to know what income and expenses are coming up in the next weeks and months.

One method is the 13-week cash flow forecast. This tracks all cash inflows (income) and outflows (expenses) on a weekly basis. Based on this data, you can forecast your liquidity for the next 13 weeks.

Scenario analyses also help prepare for different economic developments. By simulating specific business decisions (investments, hiring, M&A), you can plan ahead. You’ll know when difficulties may arise and how your cash flow will be affected. Liquidity gaps can be bridged with short-term financing.

Optimizing capital efficiency

Liquidity management helps you optimize capital allocation and efficiency. Liquidity shouldn’t just “exist.” It must be actively managed. Excess capital can be invested to generate returns, while short-term financing sources can bridge gaps.

Risk management

Risk management is another key function. Economic fluctuations, late payments from customers, or unforeseen expenses can strain liquidity. By identifying risks early, you can take countermeasures.

Cost reduction

Liquidity management contributes to cost reduction. Optimized cash flows help avoid unnecessary interest or overdraft fees. At the same time, strategic investments can put liquidity surpluses to profitable use.

Optimizing working capital

Optimizing working capital is another crucial aspect. Managing receivables, liabilities, and inventory efficiently ensures that as little capital as possible is tied up, while keeping the company solvent at all times.

Managing cash flows

Managing cash flows includes strategies like encouraging customers to pay invoices early (e.g., offering discounts) or negotiating better payment terms with suppliers. Every optimization in this area improves liquidity.

Monitoring

Cash flow monitoring plays a critical role. Effective liquidity management requires continuous financial oversight.

With software, you can analyze your cash flow in real time. You see what’s coming in and going out. This includes setting up early warning systems. You can establish thresholds for liquidity levels you don’t want to exceed or fall below. Automated systems help detect shortages and take action in time.

Hedging against financial risks

Hedging against financial risks is another key function of liquidity management. This can involve building liquidity reserves or securing credit lines.

Managing short-term funding

Finally, managing short-term financing is another critical task. When needed, you should be able to quickly access credit lines or alternative financing options to maintain liquidity.

In summary: Liquidity management ensures security, stability, and efficient use of financial resources. The goal is a company’s long-term financial health. To fulfill this role, it impacts various business areas. Which ones?

The role of liquidity management in companies

Access to sufficient liquidity is a fundamental aspect of running a business. Liquidity management is not an isolated finance topic. It affects all business areas.

- Strategic Planning: No liquidity, no investments. Companies planning for expansion must ensure sufficient financial resources.

- Operations: Salaries, rent, supplier invoices: on-time payments maintain business continuity and build trust with partners.

- Risk Management: Economic crises, unexpected costs, or delayed customer payments can be dangerous. Strong liquidity management mitigates these risks.

- Competitive Advantage: Companies with smart liquidity management can negotiate discounts, enter new markets, or finance innovation.

The key takeaway: liquidity management relies on accurate data. To manage and plan effectively, you need precise liquidity insights, ideally in real time. Only then can you confidently determine your company’s liquidity trends.

The 7-Step Liquidity Management Framework

Implementing effective liquidity management doesn't happen by accident. It requires a structured approach. Here's the proven framework that startups and scale-ups use to build robust liquidity control:

Step 1: Assess your current liquidity position

Start by getting a complete picture of your current financial state. This means understanding not just your bank balance, but your true liquidity position.

What to do:

- Calculate your current ratio (current assets divided by current liabilities)

- Determine your quick ratio (liquid assets divided by current liabilities)

- Map all cash accounts, short-term investments, and available credit lines

- Identify all upcoming obligations for the next 30, 60, and 90 days

Example: A SaaS startup with €500,000 in the bank might feel comfortable until they map out €300,000 in payroll, €150,000 in cloud infrastructure costs, and €100,000 in marketing commitments over the next quarter. Suddenly, their comfortable position looks tight.

Step 2: Build your cash flow forecast

You can't manage what you can't predict. Create a rolling forecast that shows expected cash inflows and outflows.

What to do:

- Implement a 13-week cash flow forecast as your baseline

- Track recurring revenue, invoice payments, and one-time income separately

- Map fixed costs (salaries, rent, subscriptions) and variable costs (marketing spend, contractor fees)

- Update your forecast weekly with actual data

- Extend your view with a 12-month rolling forecast for strategic planning

Real-world insight: The most common mistake? Being optimistic about when customers will pay. If your payment terms are Net 30, plan for Net 45. This buffer prevents nasty surprises.

Step 3: Define your liquidity targets and buffers

How much cash should you keep on hand? The answer depends on your business model, burn rate, and risk tolerance.

What to do:

- Calculate your monthly burn rate (total monthly expenses minus revenue)

- Set a minimum cash reserve target (typically 3-6 months of operating expenses)

- Establish early warning thresholds at 150% and 125% of your minimum

- Define your optimal cash range (minimum to maximum buffer)

Framework for startups:

- Pre-revenue: 6-12 months of runway

- Early revenue: 4-6 months of runway

- Profitable: 3-4 months as safety buffer

Step 4: Identify and manage liquidity drivers

Pinpoint the specific factors that impact your cash position most significantly.

What to do:

- Analyze accounts receivable aging (who owes you money and for how long)

- Review accounts payable terms (when you need to pay suppliers)

- Examine inventory levels if applicable (cash tied up in stock)

- Evaluate revenue concentration (dependency on key customers)

- Assess payment seasonality patterns

Action example: If you discover that 60% of your receivables are overdue by 30+ days, implement automated payment reminders and offer early payment discounts. This single change can unlock significant trapped cash.

Step 5: Optimize your working capital

Working capital optimization is about reducing the time between paying for inputs and receiving payment from customers.

What to do:

- Accelerate receivables: offer 2% discount for payment within 10 days, implement automated invoicing, follow up on overdue payments within 3 days

- Extend payables strategically: negotiate longer payment terms with suppliers, schedule payments for the last day before due date

- Reduce inventory holding: implement just-in-time ordering, liquidate slow-moving stock

- Review and cut unnecessary subscriptions and fixed costs

Impact: A manufacturing startup reduced their cash conversion cycle from 75 days to 45 days by implementing these strategies, freeing up €200,000 in working capital without taking on debt.

Step 6: Secure flexible financing options

Even with perfect planning, gaps can emerge. Establish financing options before you need them.

What to do:

- Set up a revolving credit line with your bank (even if you don't use it immediately)

- Explore revenue-based financing or venture debt for growth capital

- Consider invoice factoring for immediate cash from outstanding invoices

- Research flexible financing options like re:cap that provide non-dilutive funding tailored to tech companies

Strategic insight: The best time to secure financing is when you don't need it. Lenders and investors offer better terms when you're negotiating from a position of strength rather than desperation.

Step 7: Monitor, review, and optimize continuously

Liquidity management is not a one-time project. It's an ongoing discipline that requires regular attention.

What to do:

- Review cash position daily (takes 5 minutes with the right software)

- Update forecasts weekly with actual results

- Conduct monthly variance analysis (planned vs. actual)

- Run quarterly scenario planning sessions (best case, base case, worst case)

- Review and adjust your liquidity strategy twice per year

Automation is key: Manual monitoring is error-prone and time-consuming. This is where liquidity management software becomes essential. The right tool transforms this 7-step framework from a theoretical exercise into a practical, manageable system.

Software for liquidity management

Digital solutions have revolutionized liquidity management. Liquidity management software provides real-time insights, automated forecasts, and control mechanisms. Key features include:

- Cash position overview: a centralized view of all accounts, transactions, and balances, enabling real-time cash tracking.

- Automated cash flow analyses: visualization of cash flows, transaction allocation to teams or projects, and detailed cash flow insights.

- Forecasting: creating liquidity forecasts based on live data, running scenarios, and conducting stress tests to understand how your company would perform in different situations.

- Automated payments: software optimizes payment processes, reducing manual effort and ensuring timely transactions.

- Interfaces to banks and accounting: seamless integrations enable centralized control of all financial data. Automation ensures you always have access to accurate and up-to-date data.

By leveraging these tools, businesses can improve liquidity control, increase financial stability, and make more informed decisions. re:cap also offers a liquidity management tool with which you can manage, track, and forecast liquidity.

Top 10 Liquidity Management Software Solutions

Poor liquidity? This helps

What should you do when liquidity is running low? The sooner you take action, the better. Liquidity problems often develop gradually but with a proactive strategy, they can be avoided. Here are the key levers:

- Improve accounts receivable management: get customers to pay faster or access liquidity sooner – through shorter payment terms, early payment discounts, or factoring.

- Reduce costs: review all expenses, renegotiate with suppliers, and postpone non-essential investments.

- Explore financing options: extend credit lines with banks or look for flexible financing solutions, like those offered by re:cap.

- Activate liquidity reserves: tap into cash reserves or short-term investments if available.

- Intensify cash flow monitoring: closely track cash movements to take timely corrective action.

Summary: Liquidity management

Liquidity management is key to your company’s financial health. It ensures flexibility and stability, optimizes capital allocation, and protects against shortages.

With the right planning, efficient control mechanisms, and software tools, you stay in control of your finances and secure your company’s long-term growth.

Q&A: Liquidity management

Why is liquidity management important for startups and scale-ups?

For young companies, liquidity is often the difference between survival and running out of runway. Effective liquidity management allows you to:

- Anticipate cash shortfalls before they happen

- Plan investments without risking payroll

- Build credibility with investors and lenders

How does liquidity management differ from cash flow management?

Cash flow management focuses on tracking the movement of money in and out of your business. Liquidity management is broader. It looks at your overall ability to meet short-term obligations, factoring in cash, credit lines, and liquid assets.

What are the main tools for liquidity management?

- Cash flow forecasts (weekly and monthly)

- Liquidity ratios like current ratio or quick ratio

- Scenario planning to stress-test different revenue and cost assumptions

- Short-term financing options (credit lines, invoice factoring)

What mistakes should companies avoid in liquidity management?

- Relying on outdated data

- Ignoring seasonality in cash flows

- Not preparing for worst-case scenarios

- Overestimating incoming payments’ speed

How often should liquidity be monitored?

In volatile environments, weekly monitoring is best. In more stable businesses, monthly reviews can work but any material change in revenue, costs, or financing should trigger an update.

What’s the ROI of improving liquidity management?

Better liquidity control reduces financing costs, prevents emergency fundraising, and enables strategic moves (e.g., acquisitions, hiring).

Manage, forecast, and secure liquidity

Use re:cap to manage your liquidity. Track your cash flow in real time, forecast it, and fill short-term cash gaps with debt funding from re:cap.

Start 14-day free trial